Most AI note-takers just transcribe and summarize. Granola is an AI notepad. You jot down what matters during the call, and Granola uses your notes plus the transcript to generate summaries, action items, and next steps from your point of view. The powerful part: you can chat with your notes. Write follow-up emails, pull out decisions, prep for your next meeting — all in seconds.

I don’t promote tools lightly. This one earned its place.

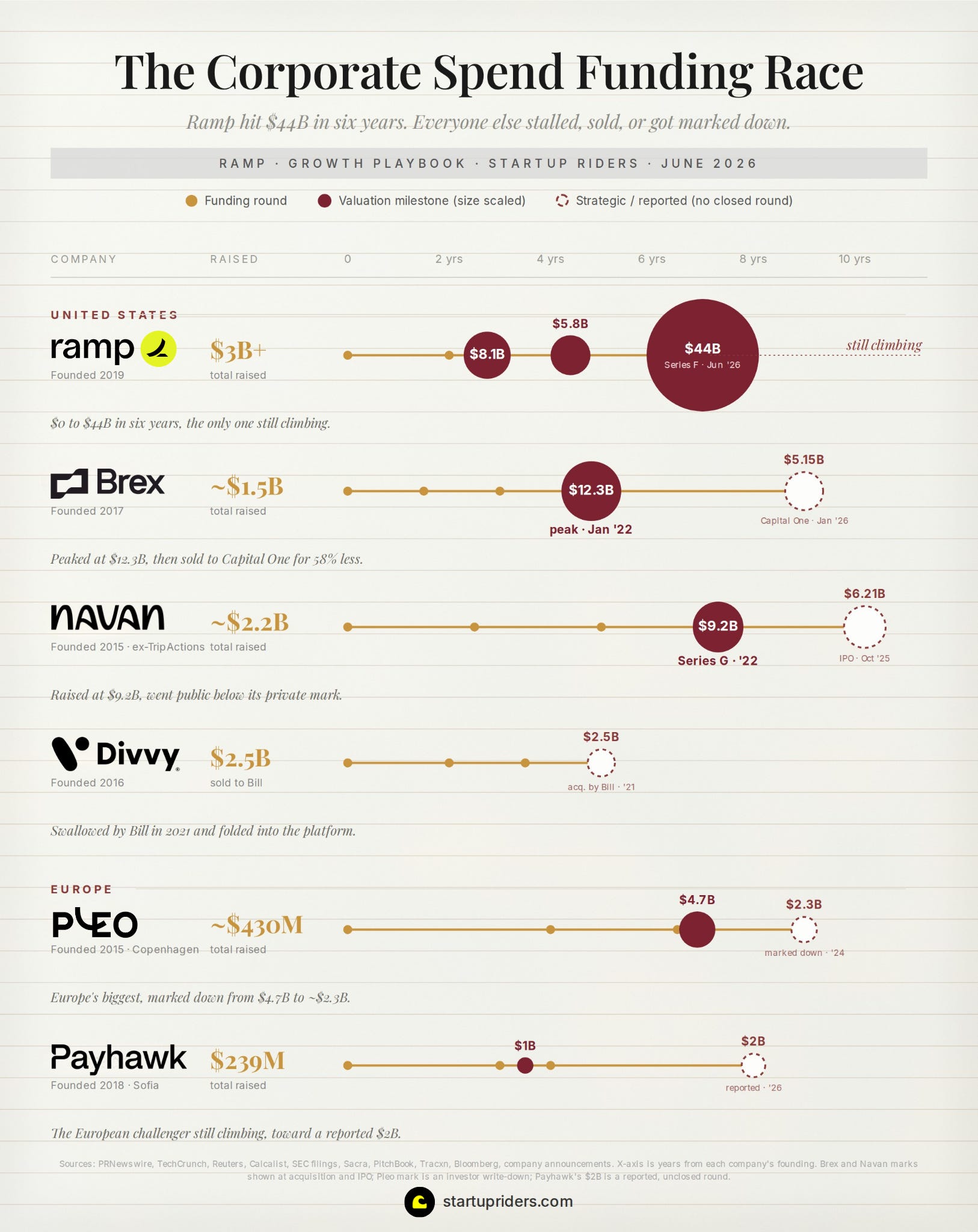

Two companies fought over the same customers with the same product for 6 years and one of them is now worth 8.5x what the other sold for, with quite the cap table:

There’s also a poetic detail in here that almost nobody mentions which is that the founders sold their first startup to Capital One, worked there, and left in 2019 to build Ramp.

So I spent the past week pulling apart 20 founder and operator interviews, every funding round since 2019, every blog post and leaked detail about how they’ve grown.

What you’ll learn

The interchange math that pays for software Ramp gives away for free

How a team of 8 engineers built an Amex competitor in 3 months

The down round they took on purpose while revenue 3x’d

The internal panic when they finally started charging for software

Why direct mail (of all things) became one of their biggest channels

The honest math under $44B (take rates, float, regulation, and the $700B government contract fight)

📐 Quick note on editorial and methodology: this analysis focuses on the 80/20 mechanics that help explain their growth (not a comprehensive profile, and not an endorsement or investment advice). It draws on 20 founder and operator interviews and long-form podcasts (Invest Like the Best, 20VC etc), plus Ramp’s own posts and reporting from TechCrunch, Bloomberg, etc. All revenue figures sourced. Reported revenue is an annualized run-rate figure, so treat directional estimates as directional.

From expense reports → autonomous finance

Ramp: $0 to $1B+ annualized revenue, 2019–2026. Valuation: $8.1B → $5.8B (the down round) → $44B. All figures sourced, annualized run-rates.

A little about how this market evolved before we get to the growth levers:

Where we come from

For decades business spend ran on 2 tools that barely spoke to each other, a corporate card from a bank like Amex or Chase that made more money the more you spent + expense software like Concur (still gives me nightmares) or Expensify that you paid for by the seat. On one hand the issuer wanted volume and on the other the software vendor wanted seats, so the finance team was left stitching the 2 together by hand every month.

Then a wave of startups tried to merge the card and the software into one platform, and for a while it looked like one of them would run the table:

Navan came at it from the travel-and-expense side and raised at a $9.2B valuation in 2022, and pushed into corporate cards and spend from there.

The category had a name (spend management) and a clear leader in Brex.

Where we are

2 things broke that order between 2022 and 2026. The first was rates going up, and once money stopped being free the fintechs that had raised at 2021 marks could no longer grow into them. 2 different things happened depending on which side of the Atlantic you were on:

Spendesk (Paris) reached profitability rather than chasing the next mark.

The second thing that happened was Ramp going the other way from everyone, taking a 28% markdown on purpose in August 2023, compounding all the way through the downturn, and re-rating from $5.8B to $44B.

Where the market is going

The fight is shifting from selling a card with some software attached to owning the system of record for every dollar a company spends, and 3 things will shape the next couple of years:

The incumbents are awake: Capital One paid $5.15B to get a modern spend platform it can aim at this exact shift and Amex and the big banks are the slower better-funded version of the same threat.

AI spend is the new battleground: Tokens are a cost line that barely existed 3 years ago and they are growing fast. They sit invisible to every legacy finance tool so whoever builds the layer that sees them has a real claim on the next decade of corporate spend.

Consolidation keeps running: With Brex gone and Divvy absorbed the independent field is thin and the survivors will keep buying whatever is left.

Now to Ramp’s origin and the 9 levers:

Act 1: The Anti-Points Card

March 2019 → March 2022 · $0 → $100M+ annualized revenue

In 2016, Capital One acquired Paribus, a price-tracker built by 2 Harvard classmates, Eric and Karim, that had saved consumers over $100M by automatically claiming refunds when prices dropped. They stayed long enough to make the acquisition work and then left in March 2019 with one of their Paribus engineers, Gene Lee.

Before writing a line of code they set themselves a goal that sounded like a joke at the time, they wanted to build a company worth $1 billion in 18 months and they reverse engineered the plan from there. Glyman confirmed the story on My First Million (well worth your time listening to the episode), and their founding engineer later looked it up and found that no New York company had ever hit $1B inside 3 years, let alone 18 months.

They got there in roughly 2 years, which is close enough, with the aim to “build a technology-driven financial services company” (email from Karim to Founders Fund in 2019):

The founding idea came from asking what would happen if your credit card could help your business spend less money. They interviewed around 100 entrepreneurs and finance leaders before launch and found something better than the original idea which is that people hated expense reports (I can vouch for that) even more than they hated wasted spend.

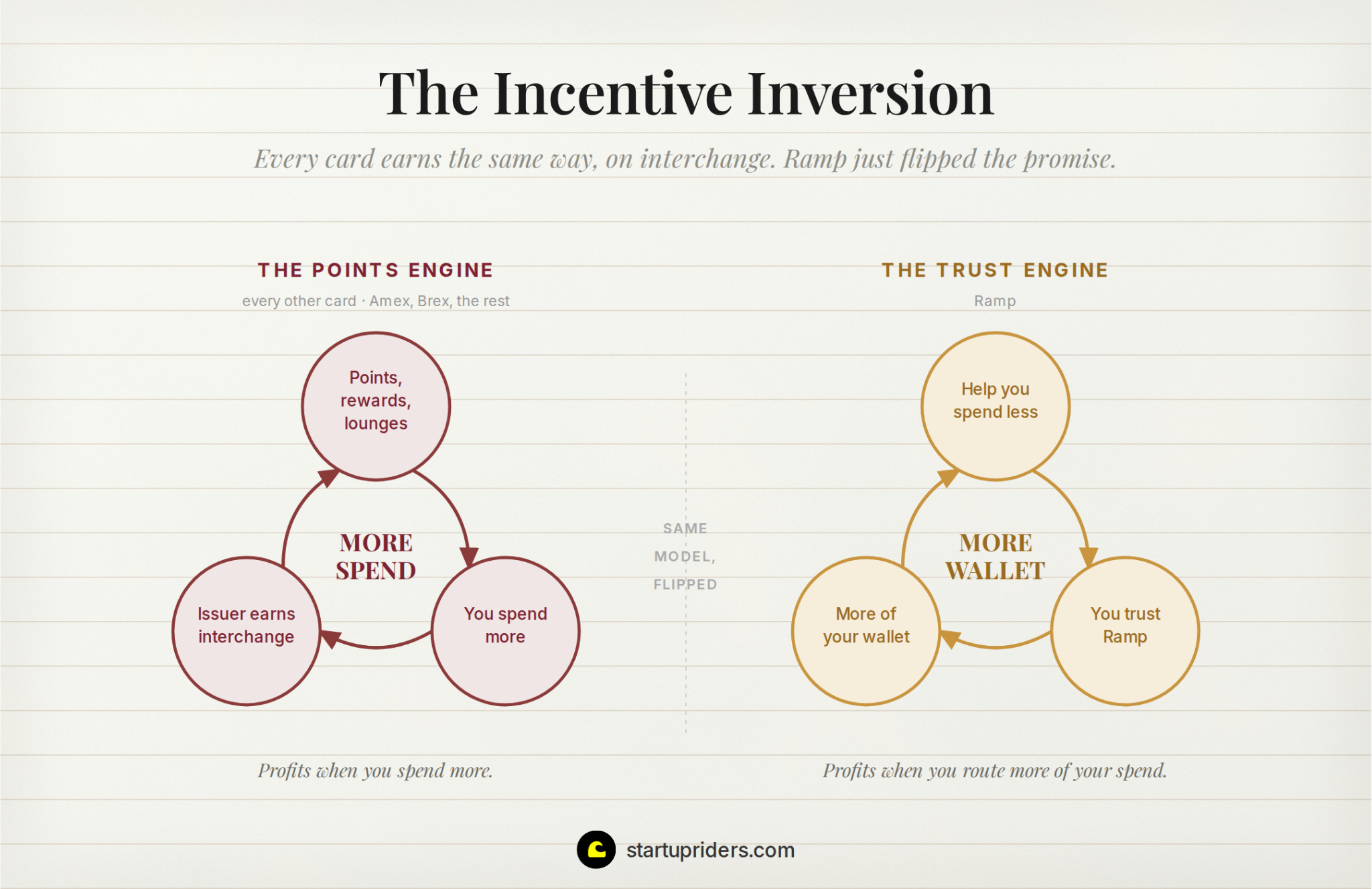

Lever 1: They made money when clients spent, and won them by helping clients spend less

“The traditional corporate card world was all about excess. When I asked people what they wanted? It wasn’t points or cash back, it was money in their bank.”

Every card company on earth earns interchange, the small cut taken every time a card gets swiped, which means every card company on earth gets richer when you spend more. The whole industry built points, rewards, lounges and steak dinners on top of that incentive, anything to make you swipe. Glyman on Stripe’s Cheeky Pint said:

“We entered into this industry where it was very profitable, but not only was it misaligned, but people were fighting over basis points.”

Ramp kept the revenue model (interchange) BUT inverted the promise:

No points, no rewards theater, just 1.5% flat cashback and a pitch that they will supposedly help you spend less

Savings insights as the product, flagging duplicate SaaS subscriptions and unused seats (i.e. you’re paying for 200 Asana seats but only 100 people log in, which they detect from Okta data, etc).

A public number to anchor it (claim to save the average business about 5% per year).

Spending less sounds like revenue suicide for a company paid per dollar spent but the bet was that it works the other way around. Every dollar Ramp saves a customer buys trust, and trust is what gets a finance team to route more of its total spend through you. You lose basis points per dollar and win all the dollars.

Hold onto the word subsidy (give away the thing your rivals charge for, get paid on the flow underneath it). In Act 3 we’ll look at what that trade actually costs though.

Lever 2: They gave the software away and let the card pay for it

“We’re a corporate card and we are the fastest growing corporate card in America, but we’re actually a productivity company.” — Eric Glyman, 20VC with Keith Rabois

Ramp’s landing c.2020

Every time someone pays with a Ramp card the store pays a small fee (usually 2-3%) Ramp keeps a slice. That slice supposedly pays for everything else, which is why the software is free:

Expense reports, receipt scanning, bill pay, approvals, accounting that updates itself

No per-user fees, contracts, interest, or late fees

The tools Expensify, Bill.com, and Concur charge for, they give away to anyone who spends on the card

The more spending crosses the card the more Ramp earns, so its job is to capture as much of a company’s card spending as it can. As Glyman put it:

“if you want to grow interchange, grow purchase volume.”

That sounds like it contradicts Lever 1, but the two measure different things:

Spending less is about the total bill, the duplicate subscriptions and unused seats Ramp cuts.

Growingvolume is about how much of the spending you were doing anyway runs across Ramp’s card instead of an Amex or a bank wire. Ramp pitches shrinking your total spend and grows its own volume at once, because the volume comes from taking share off the incumbents (not making you buy more).

As you can imagine this is probably pretty brutal to compete with, because a rival charging monthly for expense software now faces the same thing for free, basically funded by a card fee they can’t touch.

By March 2022, 2 years after launch, they were doing $100M a year with 100 to 200 employees, and Founders Fund valued it at $8.1B just before the market turned.

Bessemer State of the Cloud 2019

Lever 3: They shipped products faster than competitors shipped features

“Our culture is velocity. It shapes every process and team ritual. It’s how we develop our people. It’s our solution to nearly every problem.” — Geoff Charles, VP Product

One small team built a competitor to Bill.com in 3 months (pre vibe coding)

It cloned the core products of AmEx, Expensify, Concur, and Bill.com and gave them away free, each built by a pod of 3-5 engineers

Keith Rabois (backed Stripe, DoorDash, etc), called the pace “absolutely unprecedented in my 21 years working with technology businesses”

Some of the 80/20 choices that probably help shaped the culture:

2 kinds of engineers: After a Capital One reprimand for shipping too fast inside a regulated bank the founders split the team in 2, careful builders on the things that can’t break like underwriting and payments, and fast movers on a long leash for new products, in 3-to-5-person pods (I love this).

Hire for slope (not résumé): 1 in 3 of the first 60 hires was a former founder, and the rule was to bet on people for 10x upside rather than screen for 0 defects.

An org built to force cooperation: Product, design, engineering, and data all report to the CTO, and every spec and decision is published in the open, so teams hunt for dissent rather than sign-off and nothing waits on a gatekeeper.

Sequence new products on rails you already have: the VP Product’s rule is to pick the next product that reuses the last one’s plumbing (cards, expense, and reimbursements all share the same employee identity).

Organize teams around outcomes (not features): Each pod owns one big business result rather than a product surface (drive half of qualified leads, raise bill-pay attach rate), and has to publish an open contract laying out its goal, strategy, roadmap, and metrics so the whole company can see what it is accountable for.

One gem worth stealing is the product strategy template their VP Product shared on Lenny Rachitsky’s newsletter, which makes every team answer the same 7 Q’s before building (goal, hypothesis, right to win, metric, initiatives, risks, compounding).

By early 2022 the flywheel looked unstoppable, but then the market broke, opening the most interesting growth levers of the story:

📌 Price rises after the first 100 paid members (almost there). €19/month, €195/year - anyone in before keeps €10/€100 forever. Expense it 👇

Act 2: The Down Round

March 2022 → December 2024 · $100M → ~$500M annualized revenue

Between March 2022 and August 2023, interest rates shot up, and that resets how startups are priced. When money is cheap to borrow, investors chase fast-growing companies and (more?) happily pay a premium on their revenue. When rates jump, safer bets suddenly pay well, that premium shrinks, and the same company is worth far less without anything about it changing.

Every startup that had raised at 2021 prices now had to decide whether to defend that number. Rates hit Ramp’s actual business too, lifting the interest it earns on customer cash while raising the cost of the debt that funds card spending. They chose to reprice in public:

The framing missed that revenue had 3x across those rounds, from $100M to over $300M, so the multiple compressed from 81x to roughly 18x and the price reset to something defensible.

Brex defended its $12.3B mark for 3 years and sold at $5.15B.

By April 2024 the valuation followed reality back up to $7.65B, with revenue nearing ~$500M annualized by mid-year.

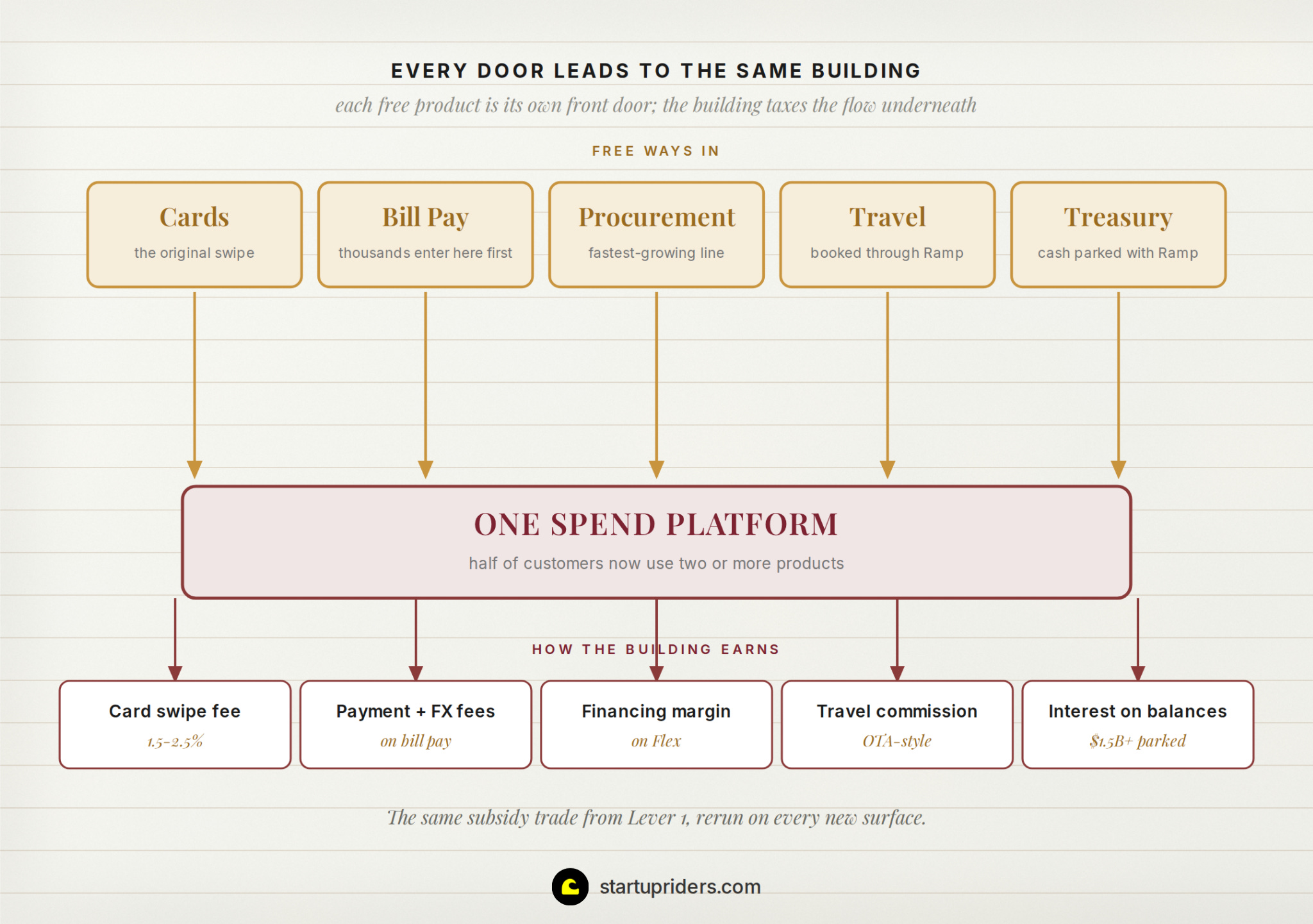

Lever 4: Every free product became a new front door

“There’s accounting firms that say, ‘We’re a Ramp shop here. If you want to work with us, we’ll bring in bill payments, treasury.’ They can manage 10, 100, 200 clients all through one platform.”

They kept adding products (bill pay in 2021, financing in 2022, procurement and travel in 2024, a treasury account in January 2025). You would expect them to land a customer with the card and then upsell the rest but each new product turned into its own front door, pulling in customers who never touched the card:

Procurement, the software that lets a company request, approve, and buy from its vendors, is now its fastest-growing line

Accounting firms started running their clients on Ramp and bringing 100-200 businesses each onto the platform, a sales team Ramp doesn’t pay for (it turned this into a product called Stack in 2026, per the Series F release)

Every product door leads into the same building and they earn a small cut of whatever money flows through it, a fee on payments, a margin on financing, a commission on travel, and interest on the cash companies park with it ($1.5B+ within a year of launching treasury). Basically this is the same trade as Lever 1 (give the software away and earn on the flow underneath it) but run on every new surface.

It shows up in two numbers, with 50% of customers now using two or more products, and Ramp apparently having more than 30% of its profit come from outside the card in 2025 (estimate plan according to Sacra for that year).

Lever 5: They started charging only when customers were already hooked

“Everyone’s a little freaked out. Are people going to be willing to pay for it? Is it going to hurt our conversion? Is it going to hurt our growth?” — Karim Atiyeh, CTO, Invest Like the Best

As they moved upmarket the free model hit a wall, since interchange on a big company’s card spend gets nowhere near covering what that company needs:

A 5,000-person enterprise wants deep integrations, audit controls, and custom workflows, and as Atiyeh put it, “we’re not able to capture any of that value for really, really large businesses because our revenue mechanism is not scaling”

So they launched Ramp Plus, a paid tier ($15 per user per month) for the advanced features, and braced for impact:

Paying customers got more demanding, leaned on the sales team, and started steering the roadmap, and growth sped up rather than slowing

Lever 6: They hunted growth where nobody was looking, or nobody believed

“The way that you find alpha is either by doing things that no one else knows about, or doing things that everyone is convinced will not work.” — VP Growth, 20VC

Ramp’s growth team runs on finding alpha (stolen from investing). Saturated channels price in their own returns, so the yield is in channels your competitors either haven’t found or have already dismissed.

The VP Growth’s (George Bonaci) favorite example is direct mail:

“It was like, why would direct mail work, junk mail to people’s homes... and it became one of our most successful, biggest channels after a few iterations.”

It worked because probably few in B2B fintech was in their clients mailbox at the time, and because the channel is absurdly scalable for experimentation (“very few channels where you can go, hey, tomorrow let’s go reach 200,000 people”).

A few more pieces of the operating system:

Sequencing doctrine (from Sri Batchu, who ran growth before Bonaci, on Lenny’s): founder-led sales first, then your first reps plus cheap targeted marketing (content, community, small events, PR), and only after all that paid and brand. Channels get more expensive down the list, and you get better at buying them as you learn your customer.

Fail conclusively (Batchu): around 30% of growth experiments work, and the sin isn’t failure but a sloppy test that leaves the question open, so the same bad idea returns every year with a new executive attached.

Events are binary (Bonaci): either take over the conference (the billboard outside, the hotel key cards, the speaker slot) or don’t go, because the lonely booth in the corner is money on fire.

Saturate winners fast (Bonaci): when a channel works, push it to its ceiling quickly, since “most things saturate probably more slowly than people expect.”

Act 3: The Token Land Grab

January 2025 → today · ~$700M → $1B+ annualized revenue

In 2025 the compounding became hard to miss:

5 valuation marks in 15 months, $13B → $16B → $22.5B → $32B → $44B

Lever 7: They gave away their data and became the news

"A lot of this data was out there, but it was the highest bidder to go and get this... we just try to open source this and let people see." — Eric, This Week in Startups

A fact about card data that most people don’t know is that hedge funds used to pay serious money for it. Aggregators bought anonymized transaction data from card companies, cleaned it, and sold it to funds trading on spend trends.

They could have sold it but instead they publish it for free on a fixed monthly schedule:

AI adoption rates by company size and industry

Spend categories rising and falling in near real time

What businesses actually buy versus what’s being marketed to them

The return on giving it away beats the return on selling it. Every release gets picked up because it’s primary data nobody else has (i.e. CNBC quotes the AI-spend numbers in their Series F coverage), and the company becomes the reference source on business spending, which is exactly the authority you want when your product is seeing and managing business spending.

As someone who writes a data newsletter, I’ll say this is the cheapest credibility engine in B2B. If your product generates proprietary data as exhaust, publishing it on a schedule can turn your ops into free media / distribution.

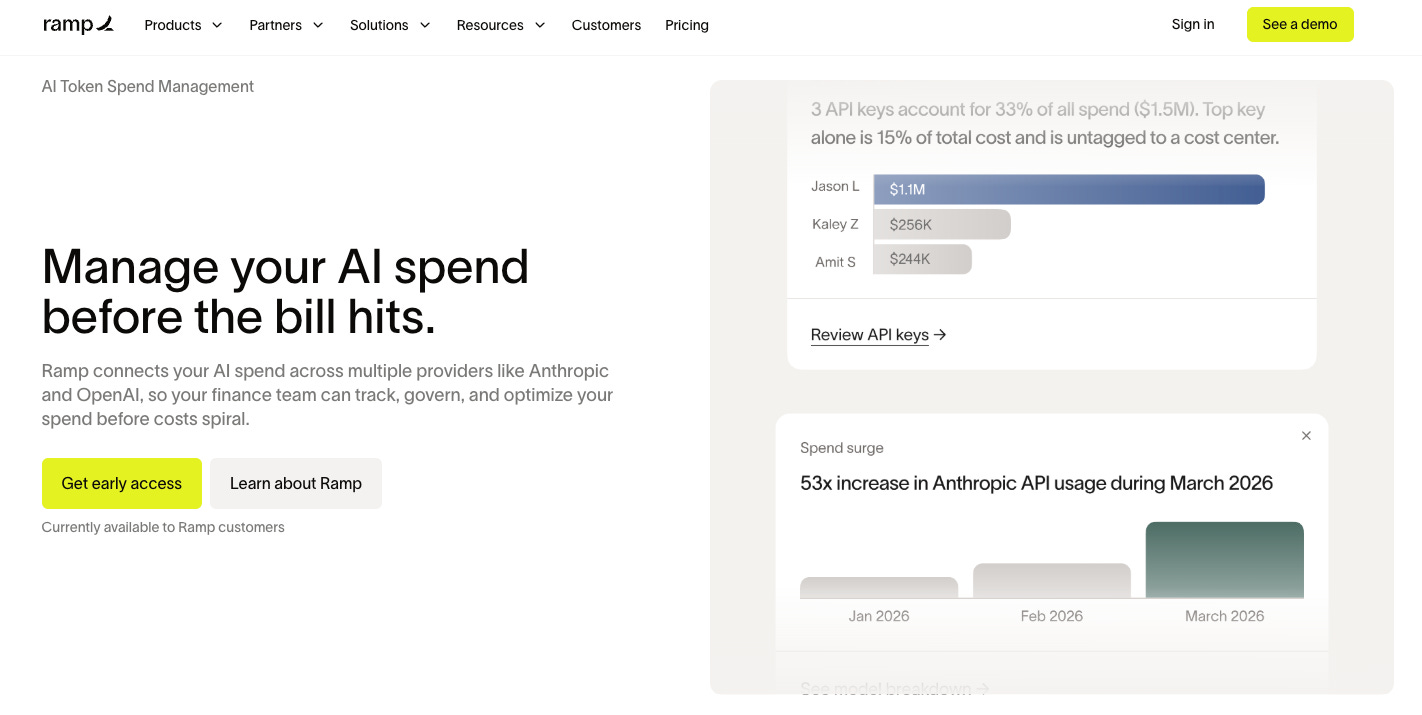

Lever 8: They chased the new cost line before tools existed for it

“For 500 years, business ran on two pillars of spend: people and vendors. In the last 24 months, a third arrived: intelligence, paid by the token and invisible to every system we’ve built to manage cost.” — Eric, Series F announcement

So in April Ramp shipped token spend management, pulling usage data straight from Anthropic, OpenAI and OpenRouter, joining it with billing data, and attributing it to teams and projects.

Their own example of the resolution they’re after reads like an APM dashboard for money (”the search team spent $340K on Claude Sonnet for the recommendation engine, up 40% since the last deploy, driven by a prompt change that doubled average token count”).

Interestingly this is kind of their 2019 playbook rerun where they find a cost line that’s growing, painful and invisible, build the visibility layer before the category has a name, give it away to capture the flow. In 2019 the cost line was card spend and the incumbent was Amex’s points machine, while in 2026 the cost line is tokens and the incumbent is a spreadsheet.

Whether token visibility monetizes like card interchange is an open question (there’s no swipe fee on an Anthropic invoice).

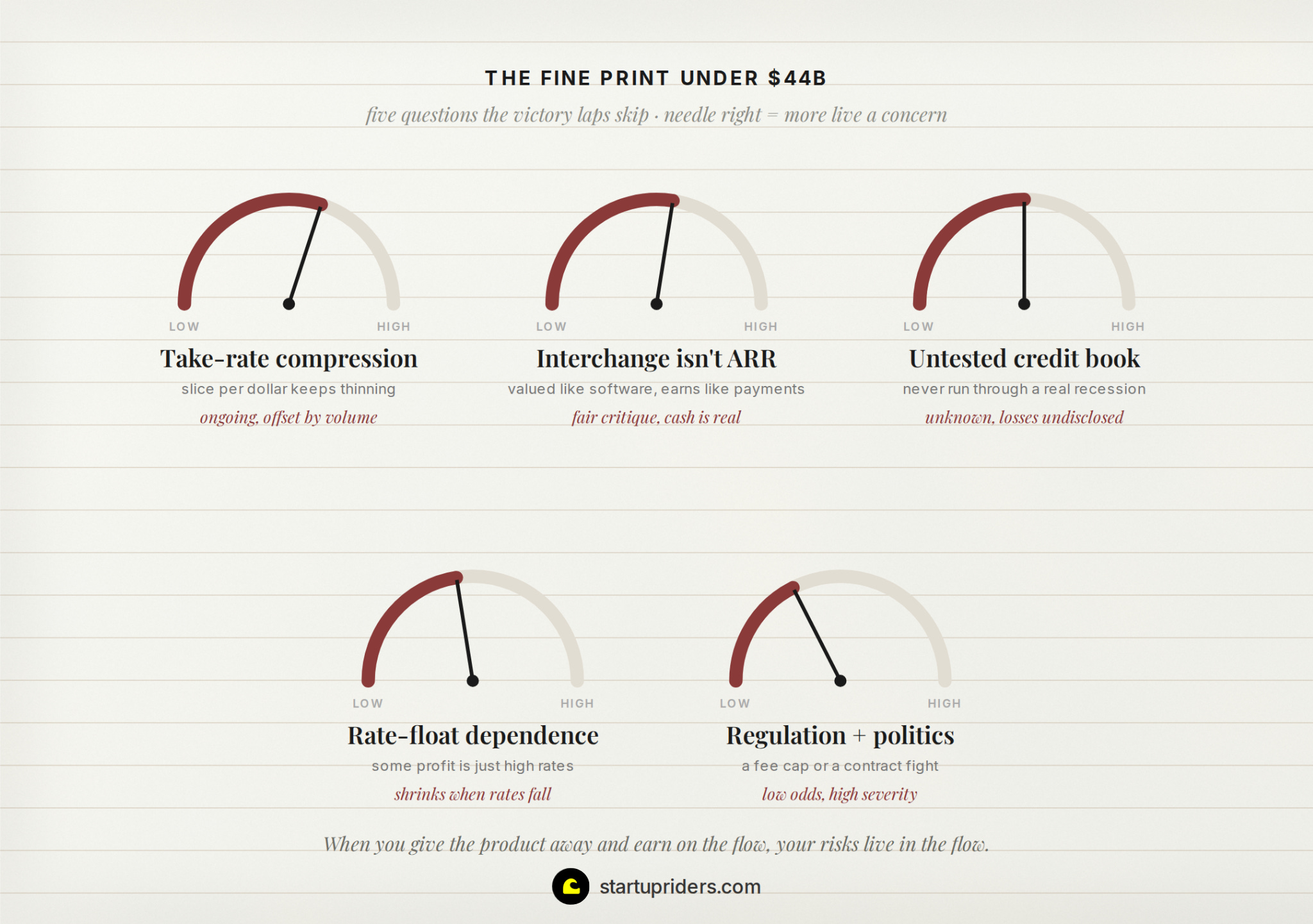

The fine print under $44B

Its also interesting to dig a little into the open questions that came up when deep-diving into this. 5 questions the bull case tends to gloss over:

1. What does Ramp actually keep per dollar?

Nobody outside the company discloses it precisely. Sacra notes the take rate is compressing for 2 reasons, more spend moving onto cheaper rails like bill pay and ACH that carry almost no fee, and bigger enterprise customers paying lower rates than startups. The slice per dollar keeps thinning but volume grows faster, which is how revenue crossed $1B. The risk sits underneath that where a business whose margin per dollar falls every year has to keep winning new volume just to hold revenue flat, and the thinner the blended rate gets, the more a software valuation starts to look like a payments one.

2. Is the revenue real “ARR”?

The skeptic's case is that Ramp is a payments company being valued on software multiples, and interchange is not the contracted, recurring revenue those multiples assume. The counterargument is that over 30% of contribution profit now comes from software and services, the revenue converts to cash unusually well, and the business throws off free cash flow at $1B scale, which most "real" SaaS companies that size don't. Both can be true at once.

3. What happens to the charge book in a real recession?

Ramp underwrites 30-day charge cards against customer cash balances, with receivables funded by Goldman and Citi warehouses. That’s elegant in good times (no revolving credit risk, no consumer-style losses) and untested at scale in bad ones, because SMB cash balances are usually what evaporates in a downturn. Loss rates are not disclosed (I’d love to see them).

4. How much of the profitability is rate float?

Treasury launched January 2025, crossed $1.5B in balances within the year, and earns interest in a high-rate world. Free cash flow positive and “underlying profitability up 153%” are real claims, and some unknown slice of them is the rate cycle rather than the product. When rates fall things will change.

5. The regulation risk.

2 exposures, both about the swipe fee that funds everything:

Ramp’s whole model runs on the 2-3% fee merchants pay on card spend. In the US there’s no legal cap on that fee for business cards, but Europe caps it near 0.3%. If US regulators ever did the same, Ramp’s main revenue source would mostly disappear overnight. It’s unlikely, but it would be fatal if it happened.

Ramp is reportedly chasing a slice of the US government’s own card program, a ~$700B pot of spend, and the way that deal was being handled has already drawn a congressional inquiry. A win would be a huge new revenue line, but revenue won through politics can be taken away by politics just as fast.

None of this is disqualifying and all of it is the price of the subsidy trade from Lever 1. When you give the product away and monetize the flow, your risks live in the flow (take rates, credit, rates, regulation), and the $44B question is whether the flow keeps compounding faster than its risks do.

20 quarters of evidence say yes for now.

5 Growth Lessons

My favorite take-aways:

They sold against their own industry’s incentive: Every card company earns more when you spend more, so the whole industry pushes you to spend more. They promised the opposite, to help you spend less, and the trust that earned is what pulled companies onto the platform.

They funded a free product from a real revenue stream rather than from runway: The software is given away, but the card’s swipe fee pays for it the same day, so free was a business model and not a countdown to the next raise (not without its trade-offs).

They waited to charge until customers were already dependent on them: Ramp Plus launched only after enterprises were running on its rails, and rather than churning, paying customers got more demanding and started shaping the roadmap, which made the product better and growth faster.

They spent their experiment budget where others had given up: example with direct mail, it looked like junk mail, which is why it was cheap and uncontested, and after a few iterations it became one of their biggest channels.

They gave away the data their product sits on: Spend data that hedge funds used to pay for (published free every month) and the press picks it up each time, which makes them the company quoted on how businesses spend.

That’s it for this week friends!

Cheers,

Ivan

P.s. If you want to help me out, the best thing you can do is share my work. 🙏

🚀 Building something in this space? We invest €100K-3M at pre-seed and seed. If you’re raising or know someone who is, please send us your deck via DM.

Great breakdown. One of the interesting things they did was they did savings reports in the early days for some companies, manually. So they did it manually (not the product) which gave them the green light to build the product after seeing that people actually value this.

→ $44B.")

Great breakdown. One of the interesting things they did was they did savings reports in the early days for some companies, manually. So they did it manually (not the product) which gave them the green light to build the product after seeing that people actually value this.

Taking a public down round while revenue tripled is one of the most disciplined moves I've seen a founder make.