Most AI note-takers just transcribe and summarize. Granola is an AI notepad. You jot down what matters during the call, and Granola uses your notes plus the transcript to generate summaries, action items, and next steps from your point of view. The powerful part: you can chat with your notes. Write follow-up emails, pull out decisions, prep for your next meeting — all in seconds.

I don’t promote tools lightly. This one earned its place.

If you have ever played around with “no-code tools” like Webflow, Zappier, Make etc, you’ll enjoy this one on n8n, the ai agent + workflow automation platform of this “no-code” tool 2.0. wave.

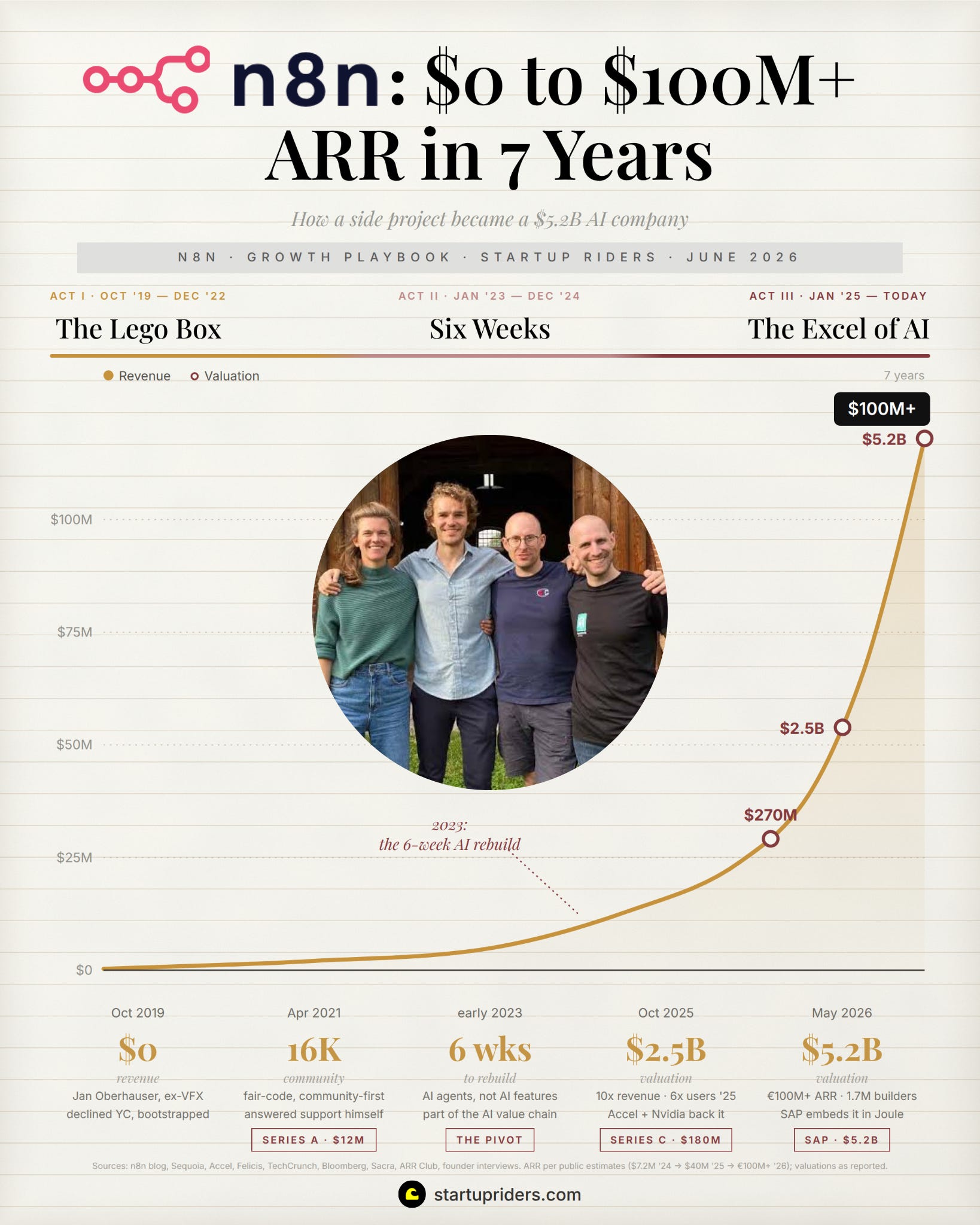

There’s a few positive anomalies that make this company special. In May of this year SAP (europe’s largest software firm) took a stake in n8n at a $5.2 billion valuation and agreed to embed it inside its own AI product.

Which is double the $2.5 billion the company was worth in October 2025, which was already close to 9x the ~$270 million it was worth in March 2025:

The tool is pronounced “n-eight-n” (I miss-pronounced it like 7x on this podcast). If you’ve built anything with AI agents in the last year you’ve probably used it. But when I ask around almost nobody knows how it grew (the founder Jan Oberhauser barely does interviews).

For its first 5 years n8n was in Jan’s own words“growing okay. Not outstanding. But it felt solid.” Then it rebuilt itself in 6 weeks and 4x’d in 8 months. I spent the past week pulling apart every founder interview, funding round, blog post, and filings I could find on how they grew.

What you’ll learn

How they grew from a side project to $100M+ ARR and a $5.2B valuation

The 6-week rebuild that 4x’d their revenue in 8 months

Why they stayed neutral on every AI model and how that became a growth engine

How giving the product away for free is what won the enterprise

Why they refused to trade power for simplicity (the 80% trap)

The “fair-code” license fight that kept developers building on it

📐 Quick note on editorial and methodology: this analysis focuses on the 80/20 mechanics that help explain their growth (not a comprehensive profile, and not an endorsement or investment advice). It draws on the founder interviews that exist (Sequoia, Accel, etc.) plus n8n’s own posts, Sacra, and reporting from Bloomberg, TechCrunch etc. n8n does not disclose revenue, so the ARR figures here are Sacra estimates or the founder’s own growth multiples. Treat directional estimates as directional.

A little about how this market evolved before we get to the 8 growth levers:

Where we come from

For most of the last decade automating work between apps meant one of 2 things:

You paid Zapier by the task to connect your SaaS tools with simple if-this-then-that rules

You paid an enterprise integration platform like Workato or UiPath a lot more to wire your systems together with the help of a consultant.

Both worked but they both also had a ceiling because simple tools were easy to start with and fell apart the moment your workflow got complicated. The enterprise tools were powerful and priced for a procurement cycle (left curious devs out).

n8n started in the gap between them. Jan’s framing of why those simpler tools kept disappointing people is interesting:

“The problem with these no-code low-code tools was always that they seem amazing in the beginning, you get a lot of value out of them, but when you want to bring it in production, you’re at 80% and you think ‘I need one or two more things’ and then you’re suddenly stuck. And then all the time you saved, you pay back 5 times to actually get it to production.”

Where we are

Then ChatGPT happened and the market split:

On one side are the model labs and agent builders that want to own the intelligence.

On the other side a fast-growing pile of vertical AI apps (each solving typically one narrow job)

And sitting between them is a question nobody had a clean answer for in 2023 which is, once you have 10 AI tools and 5 models and a dozen data sources:

what actually connects them and runsthe thing in production?

Which is the “connective layer” where n8n positioned itself. According to Sacra, the company today in 2026 serves 1,400+ enterprise customers and supports a community of 1.7 million monthly active builders, with a revenue mix estimated at roughly 55% cloud subscriptions, 30% enterprise licenses, and 15% embedded partnerships. More than 80% of workflows built on the platform now involve AI agents.

Where the market is going

3 things will shape the next couple of years:

The work splits in 2: Jan’s distinction is that some enterprise work is deterministic where there is one correct outcome and anything else is a mistake (compliance checks, billing, data updates). The rest is non-deterministic where judgment and context shape the answer (triaging a ticket, drafting copy, deciding what to do with an anomaly etc). Most AI tools handle one or the other but n8n is supposedly built to mix code, rules, and agents in the same workflow.

Protocols standardize the plumbing: they call Model Context Protocol “the HTTP of AI workflows,” and sees n8n as the orchestration layer between MCP-connected services, agents, and tools.

The hyperscalers circle: Sacra flags the risks here that I tend to agree as AWS, Google, and Microsoft can bundle workflow automation into their AI services and subsidize it. The counter-move as we’ll see is the SAP deal and a self-hosting story the hyperscalers might struggle to copy.

Now lets dive into how they grew.

Act 1: The Lego Box

Oct 2019 → 2022 · $0 → “growing okay, not outstanding”

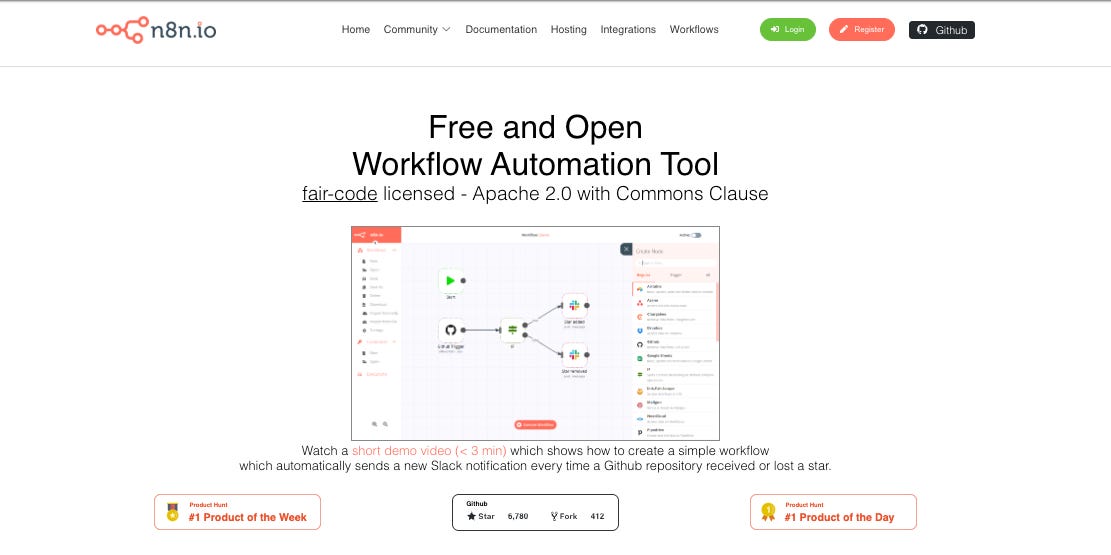

n8n website in early 2020

n8n started with a visual effects artist who was bored of doing the same thing twice.

Jan was a compositor (the person who combines the computer-generated 3D with the filmed footage and makes it look real). He got bored, moved into a more technical role as a pipeline technical director and spent his days building tools to make the artists around him faster.

Which is the job-to-be-done the company seems to comes from:

“Those people [were] very smart, very well paid and quite technical, but they were always reliant on me or other people like myself to actually do the things they wanted to be done. They could have had so much more impact if they would have been empowered, and they weren’t. I think n8n is doing exactly that.”

At a later startup he realized he was spending most of his own time rebuilding things that already existed:

“I spent probably 90% of my time reimplementing things that have been implemented before. Get something on GitHub, send a message to Slack. Each of those pieces have been implemented millions of times before by almost every developer out there, and this is never the most fun thing to do.”

So he set out to build a box of reusable Lego blocks for that plumbing, and free himself to spend time on the part that was actually specific to his problem.

He built n8n nights and weekends across roughly a year while working at a second startup to pay rent because as he puts it plainly, “I already had wife and one child back then, so I obviously needed some food and some shelter as well.”

He’d started coding at the beginning of 2018, a soft launch came in June 2019, the proper one in October. The name is actually a numeronym for “nodemation” (node plus automation), the 8 standing in for the 8 letters between the two n’s.

He’d been invited to Y Combinator and turned it down because he didn’t want to leave Berlin or incorporate in Delaware. Sequoia and firstminute co-led a $1.5M seed in March 2020 anyway, with Felicis leading a $12M Series A a year later. By that point the community was around 16,000 developers.

Growth Lever 1: They gave the product away and treated support as the product.

“I knew the product was very imperfect when I launched. The only way you can still make sure people are happy is if you make sure they have the best experience possible when they run into one of those issues.”

The product was free and self-hostable from the start.

One of the first people Jan he hired was a community person, before it made any obvious financial sense, purely to write documentation, run the forum, answer questions fast etc. He chose a forum over a Slack or Discord on purpose:

“These people have a problem, I answer that question once, maybe 3 times. At least I don’t have to answer it 50 times. That allowed us to scale.”

The bet was that a free product with rough edges plus genuinely fast, genuinely caring support produces users who leave a problem feeling better than if they’d never hit it because they now trust that someone will unblock them, and those users tell other people, they write tutorials, build integrations etc (similar flywheel to the one we ran at Facebook, explained in this playbook).

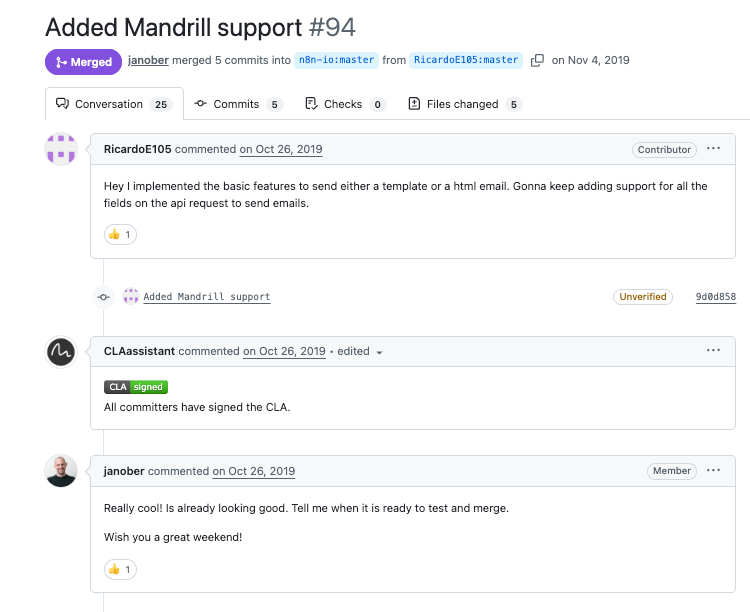

The clearest example is a developer named Ricardo, based in the US, who found n8n on Product Hunt at launch, and built one integration for fun. Jan reviewed it and gave feedback, he built another, and another. In the end he contributed 56 integrations before n8n had the money to pay him. As soon as it did, Jan hired him and he’s still there, and was for a long time the only n8n engineer in the US.

Growth Lever 2: Refused to trade power for simplicity

“We have a steeper learning curve. You can only make the product so simple, because if you make it even simpler, you have to give something up for it, which is flexibility and power. And that was always at the center of n8n.” (Jan, Accel)

Everyone else in the last automation wave chased the same goal which was to get a beginner to their first working automation in 5 minutes. But n8n optimized for the other end which is the moment a workflow gets complicated and wouldn’t sacrifice that power to smooth out the first 5 minutes.

An example of this, under the drag-and-drop canvas there’s a real code editor, so when you hit something the buttons can’t do, you write a line of JavaScript or Python and keep going, whereas Zapier and Make lock the code away and cap you at what their menus allow (so n8n leaves the door open lets say).

It matters for growth because every easy tool tends to have the same leak, which is it wins you in week one, you build something real, you hit its ceiling (the 80% trap), and you move to a “proper” platform, so the tool that got you loses you right when you technically became “valuable”.

I think their goal was to set the ceiling is high enough that you never need to leave, so:

A solo builder and a 500-person enterprise can technically use the same product.

The people outgrowing Zapier and Make now move to n8n because there’s nothing left to “outgrow”.

And the same canvas that sends for example your first Slack alerts later can run your company’s AI agents (or at least that’s their plan now).

As an example imagine a developer finds n8n on GitHub, runs it for free, builds something real, then pushes their company to pay as usage grows. The steeper curve is a side effect of keeping that power available and it self-selects for these people (aka technical enough to build serious things and the ones who get a tool into a Fortune 500).

Growth Lever 3: They never changed the rules on the community.

"I'm not building n8n and giving it away for free because I'm a good person. I actually want to build a business around it. I want to make sure I can get paid, and all the other people can get paid as well." (Jan, Sequoia)

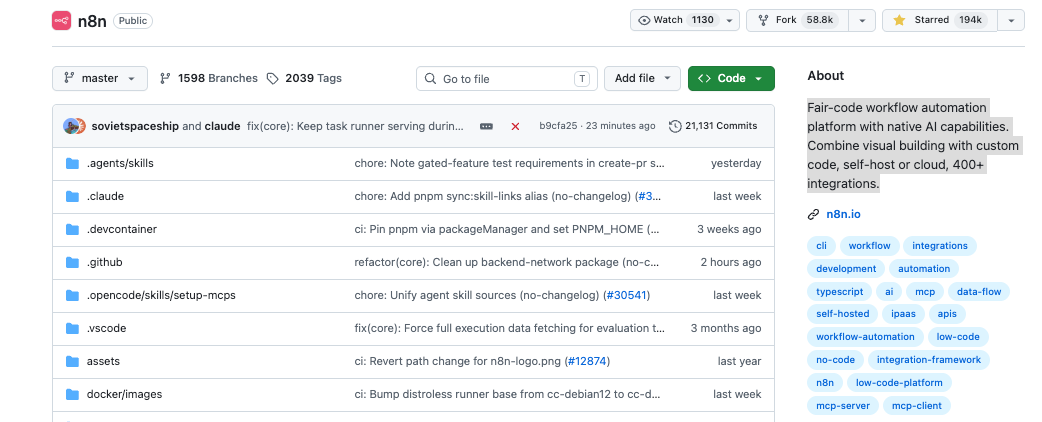

n8n is one of the most-starred projects on GitHub (194,000 stars, roughly a top-40 project globally), and Jan is careful to never call it open source.

It didn’t start clean though as n8n launched under Apache 2.0 with a Commons Clause modifier, which broke the technical definition of open source and made some people unhappy. But instead of fudging it, the founder dropped the words “open source” and coined his own term, “fair code.”

What fair code actually means:

The code is visible and free to use, even in production, even inside a Fortune 500.

The one thing you can’t do is take it and sell a hosted version.

It is a growth lever because a developer won’t pour months into building on a free tool, contributing integrations, and getting their company to standardize on it unless they trust the rules won’t change once they’re locked in.

And by 2023 developers had every reason to expect the opposite because a run of open-source companies (i.e. MongoDB, HashiCorp, Redis and others) got big then quietly changed their license to block cloud providers from reselling them and their communities turned on them.

“People didn’t hate it because of the license the companies chose. People were mainly angry because the company changed the rules. So I thought, I’m just very honest and upfront about it from the very beginning.” (Jan, Sequoia)

I imagine that honesty was an unlock because the founder said out loud that n8n was a business and would stay free under clear terms, so developers built, contributed, and standardized without watching their backs. So the free tier stayed genuinely free, the commercial license funded everything, and there was no betrayal in between.

Act 2: Six Weeks

2023 → Dec 2024 · the rebuild that changed everything

By early 2023 n8n was a solid, growing, community-loved dev tool.

Then Jan got scared:

“When AI came up the first time, I honestly was a bit scared, because what was clear is it’s changing the whole game. Things I just months before thought would be impossible suddenly became very easy.” (Jan, Accel)

What tipped him off was seeing Pinecone raise $30M, which made them ask why a vector database was suddenly so interesting.

“What they were in the past, they were the vector database. What they became, they became a deep database for AI. That’s where I said we have to do something very similar within n8n.”

Growth Lever 4: They spent 6 weeks turning n8n into the place you build AI.

“Enhancing the product with AI features would give us a 10, 20, 30% boost, but it wouldn’t allow us to grow 10X. So we took a step back and realized, if we really want to be successful, we have to allow people to use n8n to build AI applications, to become part of the value chain.”

The “easy” 2023 move (the we saw many SaaS incumbents execute on), was to add AI features. n8n already had an “OpenAI node” you could call over the REST API, like everyone else, but Jan did the math out loud (quote above) and refused that path.

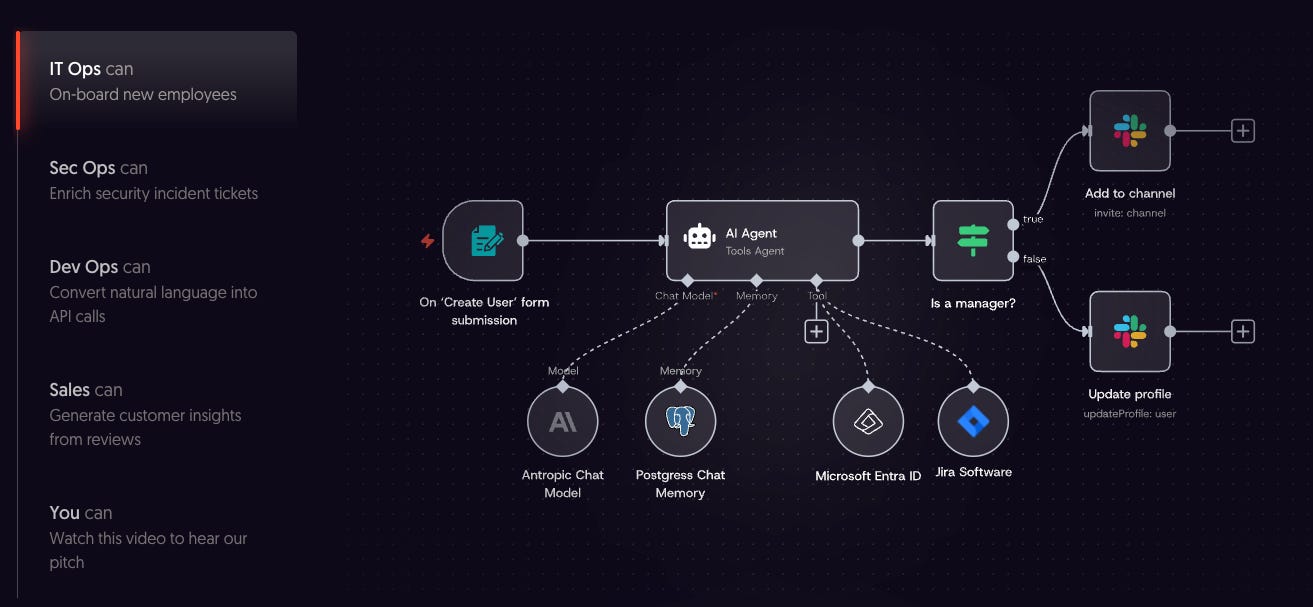

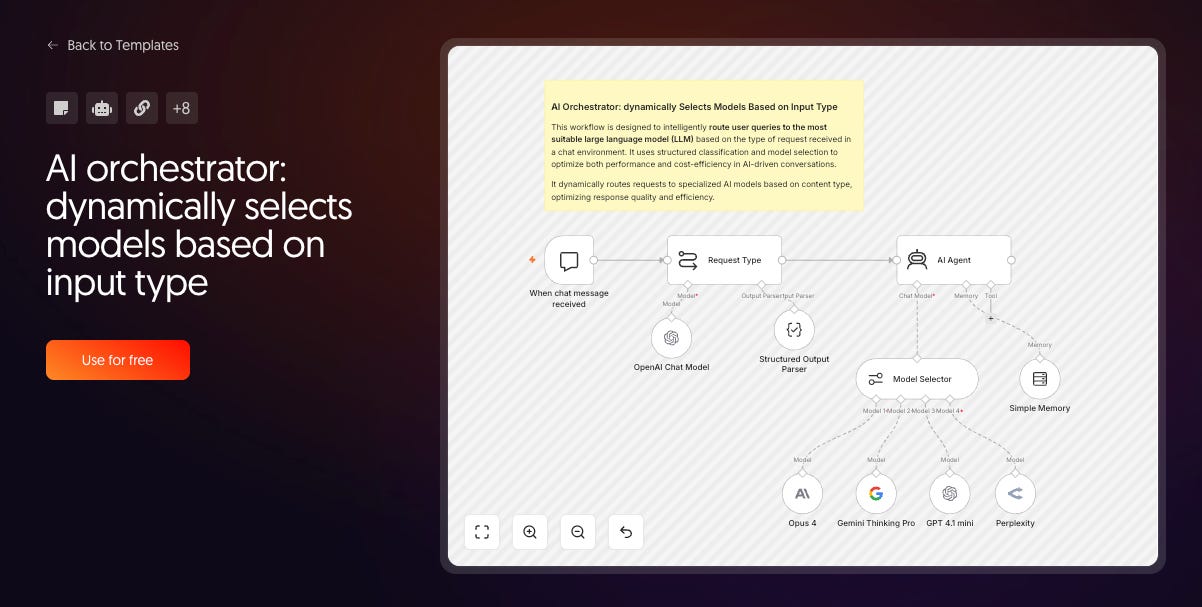

Instead of one node that calls a model they started letting people assemble real agents:

Swap in any model

Attach a vector store

Add memory

Chain multiple agents together

Wire all of it to the hundreds of integrations n8n already had

The plumbing AI needs (connect to data, transform it, send it somewhere, trigger something) was the plumbing they had been building for 4 years. From decision to release was about 6 weeks done by Jan plus “one and a half” engineers, a tiger team on purpose (“smaller teams are actually much more helpful”).

Jan, who calls himself “not the best coder in the world,” went back to full-time coding and called it one of the most joyful stretches in years. The result was revenue quadrupled in the 8 months.

Apparently the launch was “underwhelming,” and the community Jan had spent 4 years building got a bit nervous, “concerned that the product they loved was being replaced instead of enhanced.” It took a year of listening and steady building to win them back but in his words: “It’s almost like we launched again.”

Growth Lever 5: They refused to bet on any model, so every launch helps them.

“I don’t know what LLM is going to win the race in the end… But that’s the great thing about n8n. We don’t have to care, because you can use whatever is best for your use case.” (Jan, Sequoia)

n8n connects to every model from every provider and bets on none of them, here’s why that’s a growth lever:

The labs do their R&D for them: burning billions to ship the next model, makes n8n better with every upgrade.

Neutrality is usually fatal (except here): supporting every model means paying for every model’s inference which sinks most companies but n8n sidesteps the bill entirely because customers plug in their own API keys, so n8n keeps the subscription and doesn’t pay for a token (that’s how they hold 75%+ gross margins).

Swapping models is easy but leaving n8n isn't so easy: a cheaper or better model comes out, the customer changes one setting and every workflow they built keeps working. So they switch models whenever they want, and n8n is the thing that stays underneath all of it. So while the labs fight each other on price n8n keeps the subscription either way.

Fragmentation is a tailwind: because more models, more providers, more tools means more stitching, and stitching is the job. Over 80% of workflows on the platform already run AI agents and the messier AI gets, the more you need the neutral layer holding it together.

Growth Lever 6: They deleted their lead-generation goal and let the community pull in the enterprise.

“We removed the lead goal. We exchanged it with an adoption [goal] of large organizations, went all in in the community.” (Jan, Sequoia)

n8n’s marketing team apparently had always been measured on leads but the problem was that the team was great at adoption but always fell short on leads. So they kept pulling effort out of community growth to hit a lead target, which killed the long-term compounding. They decided to remove the goal entirely.

“It doesn’t matter for me if we have 10 or 20 million less ARR end of this year. What matters is we keep to the market.” (Jan, Slush fireside)

The logic underneath is a sequencing claim about how you actually reach the enterprise:

“Through the smallest builders, we get into the largest organizations. If you focus very heavily on enterprise only, you can never go downwards again. Google started the same way. Microsoft as well.”

So they fed the top of the funnel with events, content, and community programs. The flywheel that did the real work was creators, as the Felicis profile puts it, community members started making YouTube and LinkedIn content about building AI on n8n, and:

“the more content people create, the more other people want to create content, the better it gets ranked, and then everything started to explode.”

In 2025 users grew 6x and revenue 10x in 1 year. Jan told Sequoia the company added 4 times the revenue in 8 months that the first 5 or 6 years had built. Sacra estimated ARR around $40M by mid-year, and it has since crossed €100M+ post-SAP.

The money followed. A €55M Series B (Highland Europe, ~€270M), then a $180M Series C (Accel, $2.5B, with Nvidia’s venture arm joining), then SAP at $5.2B.

“What was Excel 15 years ago for spreadsheets, n8n should become the same for AI. Empowering everybody to use AI to the fullest, from private use cases, to SMBs, to the largest enterprises, up to government organizations.” (Jan, Accel)

Growth Lever 7: The community pre-built 10K workflows, became the onboarding + top of funnel.

“We wanted to fix the ‘blank canvas problem’... somebody coming into our tool and wondering where to go from there or what to automate first.” (Tanay Pant, n8n’s Head of Developer Relations, 2021)

They also built a library of 10,245 ready-made workflows (sourced from the community of course) to deal with the “blank canvas” problem, pretty cool how each one is importable in one click.

Brought several advantages / fuelled their growth in a few ways:

It gets a new user to a win in minutes: search the thing you want, import a working version, plug in your keys, done.

Every template is a page that ranks on Google: 10K+ each one targeting a specific search like “n8n Notion sync” or “build an AI agent that does X.” So the community writes them, n8n’s search footprint grows without n8n paying for content. Whole third-party sites now exist just to re-host n8n templates for the traffic.

They pay people to feed the library: they run a creator and affiliate program so contributors get featured and earn for submitting templates. The library grows faster than any in-house team could write it, and the people building templates become the people selling n8n for them.

It caught the AI-agent search wave at the moment of intent: when everyone started searching “how do I build an agent that does X” they already had a template for X.

Also interesting, today over 80% of workflows on the platform now run AI agents.

Growth Lever 8: They let companies keep it fully in-house, which won the buyers who won't touch the cloud (including SAP)

“It’s more or less a difference between renting and owning. You really own it, and you can decide what’s important and how you want to move forward.” (Jan, EU-Startups)

Because n8n is fair-code and self-hostable a customer can run the thing on its own servers. For the most regulated buyers that’s a critical purchasing factor:

Pure SaaS: the vendor can switch you off and your data lives somewhere you don’t control.

Self-hosted n8n: you own it, you run it, nobody outside can touch it.

The biggest budgets with the lowest tolerance for risk.

SAP made the same call, at scale:

It’s the back office for 99 of the 100 biggest companies on earth, all needing AI they can run on mission-critical paths with full control and audit trails.

For n8n this is enterprise distribution (SAP hands it to the world’s largest companies), and n8n hands SAP an orchestration layer it didn’t want to build.

Lets see where the company goes next, excited to see them grow (from Europe!).

5 Growth Lessons

My favorite take-aways:

Built for the pain they lived: it was born out of one VFX engineer’s frustration (”smart people, always reliant on me”) + going deep + iterating fast.

Let the product build AI: adding an AI feature was the 30% move but becoming the place people build AI was the 10x move, they rebuilt for it in 6 weeks.

Stayed neutral on the bet everyone else was making: nobody knows which model wins so they bet on none of them and every launch makes it stronger now.

Deleted the metric that was eating or distracting them from their best channel: killed the lead-gen target and ate probably a bunch of ARR (hard trade-off) to keep feeding the community which was the thing actually compounding.

Sold ownership: “You own it and nobody can switch it off” was a big accelerant.

n8n now joins the $100M ARR Breakout Club, see the full Startup Riders Growth Index of the fastest-growing private tech companies past $100M ARR.

P.s. If you want to help me out, the best thing you can do is share my work. 🙏

🚀 Building something in this space? We invest €100K-3M at pre-seed and seed. If you’re raising or know someone who is, please send us your deck via DM.

The SAP partnership proves that when you build an incredibly solid tool that developers actually love, top-down enterprise distribution follows naturally.

![Seed $1.5M (Sequoia + firstminute, Mar 2020) · Series A $12M (Felicis, Apr 2021) · Series B €55M (Highland Europe, Mar 2025) · Series C $180M (Accel, Oct 2025, $2.5B) · SAP strategic (May 2026, $5.2B). Total raised $240M. — source: Crunchbase / n8n]](https://substackcdn.com/image/fetch/$s_!_0EW!,f_auto,q_auto:good,fl_progressive:steep/https%3A%2F%2Fsubstack-post-media.s3.amazonaws.com%2Fpublic%2Fimages%2F03dabaee-1550-4574-816c-39221f8ac288_1688x882.png "Seed $1.5M (Sequoia + firstminute, Mar 2020) · Series A $12M (Felicis, Apr 2021) · Series B €55M (Highland Europe, Mar 2025) · Series C $180M (Accel, Oct 2025, $2.5B) · SAP strategic (May 2026, $5.2B). Total raised $240M. — source: Crunchbase / n8n]")

This was comprehensive and really valuable. Thanks for this. Could you do Cursor, Supabase, Blotato next?

The SAP partnership proves that when you build an incredibly solid tool that developers actually love, top-down enterprise distribution follows naturally.