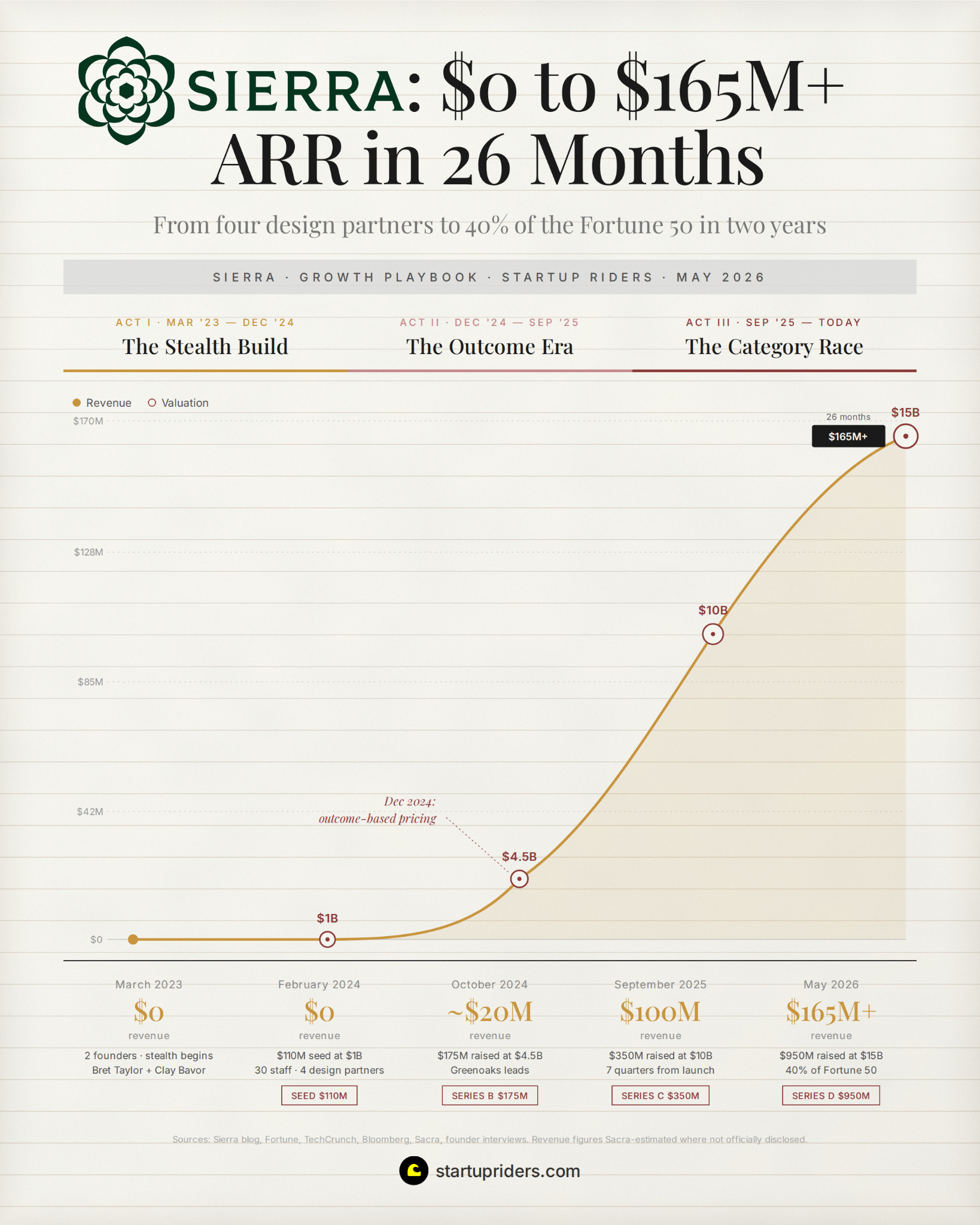

It’s been a huge week for Sierra, who just announced a fresh $950M round at a $15B valuation in an attempt to win the enterprise segment for customer experience.

It's also a unique growth story because Bret Taylor is running it (ex Meta CTO, Salesforce co-CEO, OpenAI chairman).

ARR has gone from $20M → $165M ARR in a little over 1 year, and they serve 40% of the Fortune 50, 2 years and one month after public launch, which is the fastest enterprise software scaling curve I’ve ever charted.

So I spent the past week pulling apart 22 founder interviews, every Sierra blog post, every customer case study, and every funding round.

The 4 customers Sierra picked to break and build the product

Why they played for the Fortune 500 quadrant

The product and pricing choices they made to accelerate time-to-live

The land-and-expand play that turns customer service into a $5M+ ACV

How they named the category before Salesforce woke up

📐 Quick note on editorial and methodology: this analysis focuses on the 80/20 mechanics that help explain their growth (not a comprehensive profile, and not an endorsement or investment advice). Based on 22 interviews (Lenny’s Podcast, Acquired, Sequoia, etc.), plus reporting from TechCrunch, Bloomberg, Fortune, Sacra Research, plus Sierra’s own blog + case studies. All revenue figures sourced. Treat directional estimates as directional.

Act 1: The Stealth Build

The same week ChatGPT launches in November 2022, Bret Taylor walks out of the Salesforce co-CEO office for the last time. In his words:

“Nerd sniped me a little bit, I just couldn’t stop thinking about it.”

He then starts building again (an app for his daughter), a “choose-your-own-adventure” game, but the AI writes the next chapter based on her decision. He had written technology that wrote a book in real time, which turned his model of what computers were upside down.

The two had been trying to work together for 15 years. Apparently they had “a monthly poker game that happens roughly twice a year.”

Clay was a year ahead at Google in the APM program, they worked on Maps and Gmail and Drive in adjacent buildings during the early 2000s, but Clay stayed at Google for 18 years.

We won’t spent time on Bret’s trajectory (well covered), but in a nutshell, he left for Friendfeed, then Facebook, then Quip, then Salesforce, then OpenAI’s board chair seat. Every 2 or 3 years one of them would float the idea of building something together but it never aligned.

Until early 2023, when they startedSierra. At that time most AI startups were going horizontal (remember all the chatgpt API and everyone wrapping it in a UI?). But these two went vertical and they went narrow (at first), and picked customer service.

Lever 1: They sold to people who already trusted them.

“Until you have a representative happy customer, your ivory tower view of what your product could be and should be is probably wrong. Two happy customers becomes four becomes ten.”

By mid-2023 every Fortune 500 CIO was getting pitched by 20+ AI vendors every week because product readiness and model capability had stopped being the bottleneck.

Sierra went around the new war for attention by going “around it” and selling first to people who trusted them (cashing-in their “trust piggybank”).

Between both founders they had 30+ plus years across 3 of the companies that literally built modern enterprise SaaS, in jobs where buying decisions came across the desk every week. So, they knew some people.

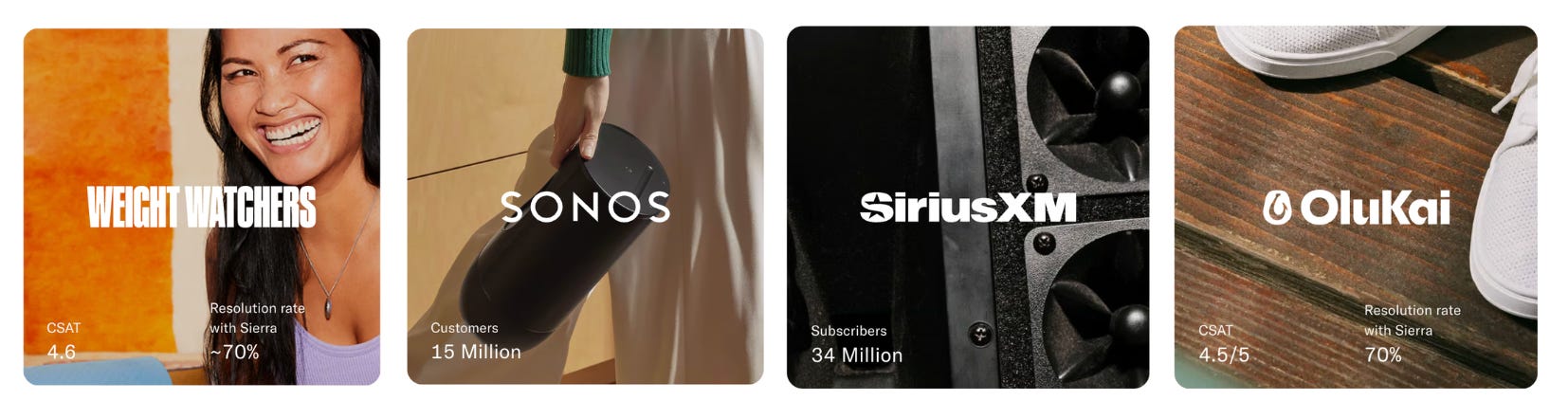

They recruited 4 design partners to build the product in stealth for 11 months.

The four were:

WeightWatchers: was inside a corporate restructure and needed customer service costs to come down fast.

SiriusXM: had 34 million subscribers and a legacy IVR that customers hated, which meant any AI improvement showed up in NPS the same week.

Sonos: has Black Friday surges that hit 10x normal volume.

OluKai: was the smallest (on purpose). A sandals brand with low ticket volume and a customer base obsessed with the brand voice, which forced Sierra to build agents that could hold a personality at production scale.

What’s smart and interesting in their decision on who they picked for this phase, is that they intentionally chose customers who’d force the hardest constraints on the product.

And because they had chosen the intersection of that type of customer + the fact that they already knew and trusted them as partners, gave them room to ask for things (i.e. full IVR data, a senior CX exec assigned full time, etc) that no cold pitch usually gets.

Most competitors in 2023 had bigger models, more engineers, faster shipping, etc but lost the first 18 months of the enterprise AI race because they were still trying to get on the calendar of people while Sierra had been building with for almost 1 year.

Hold onto the word alignment here because the first lever is alignment between Sierra and the 4 customers who would shape the product, and every lever after this one is the same architecture pointed at a different stakeholder.

Lever 2: They let unit economics pick the customer list

“Understand which specific math problem your product solves, and pick the customer segment where the math is most obviously true”

“The price of a phone call is $10, maybe $20 depending how long the conversation is. If you think about the average revenue per user of Google, they literally just can’t afford to do it.”

A human-handled customer service call costs roughly $10 in the US (load in agent salary, benefits, supervision, software, and the six to twelve minutes the call takes). Sierra’s per-resolution cost sits somewhere between 10 cents and $1 depending on conversation length.

Once customer service is 100x cheaper, it stops being a back-office cost and starts being something companies can actually compete on (faster resolutions, better experience, cheaper than competitors).

The trick is that every Sierra customer gets roughly the same percentage savings (~90%), so the % doesn’t really tell you anything about which customers are good targets. What matters is the absolute dollar number, and that depends entirely on company size. A small company saving 90% of a small bill is still a small number. A massive company saving 90% of a massive bill is a number that lands on the CEO’s desk. Here’s a quick example with 3 companies + 3 scales:

Regional retailer, 500K customers → ~$10M of contact-center spend → AI saves ~$9M. Real money for a small business but not really enough to move a board or accelerate a sales-cycle + integration.

Mid-market subscription, 5M customers → ~$75M of spend → ~$70M saved. Significant, but the deal still has to fight for attention against 20 other cost-cutting initiatives every quarter, similar to above.

Fortune 500 telecom, 50M customers → ~$1.2B of spend → ~$1.1B saved. This is a strategic priority that lands on the CEO’s desk and gets fast-tracked.

The threshold probably sits around $100M in annual contact-center spend, because below that the deal might still close but on a slow enterprise cycle alongside other vendor evaluations.

Each of Sierra's 4 design partners turned into a unit-economics laboratory for proving the model to the next wave of Fortune 500 buyers:

WeightWatchers evaluated on containment rate

Sonos on time-to-music-playing

SiriusXM on subscription saves and upgrades

OluKai on customer satisfaction during the brand’s signature aloha moments

With this early liquidity quality, they raised $110M from Sequoia and Benchmark at just under a $1 billion valuation. Eight months later (October 2024) they raised a Series B at a $4.5B valuation, with production volume scaled into the next wave (i.e. Cigna, ADT, SoFi, Casper, etc), and ARR tracking toward $20M.

Act 2: The Outcome Era

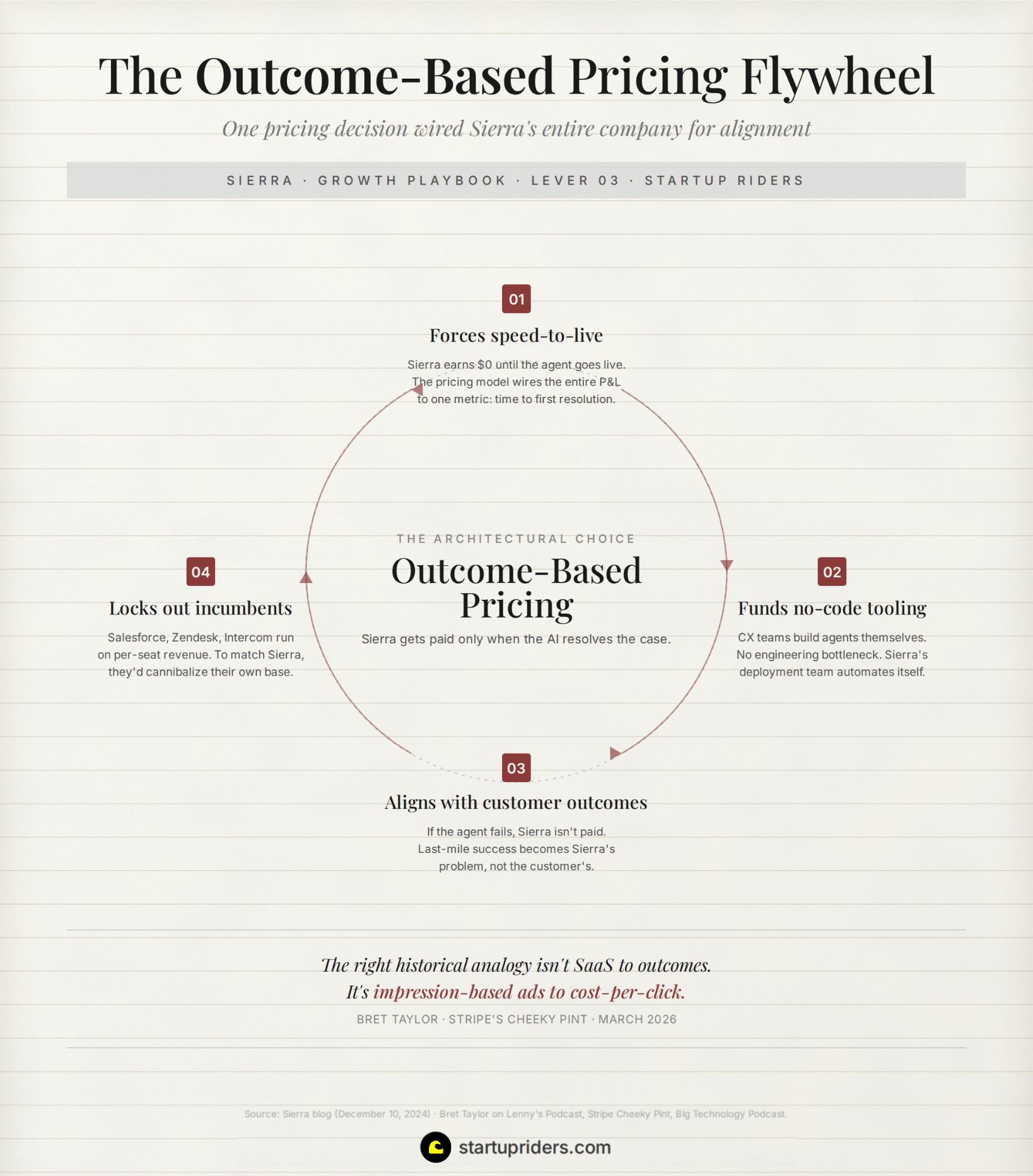

In December 2024 they published a pricing manifesto explaining how Sierra would charge customers going forward, and the answer was that they would only get paid when their AI agent successfully resolved a customer service case.

Lever 3: They only got paid when the AI worked.

Business model transitions are harder (for incumbents) than technology transitions

The model itself is simple:

Sierra’s AI agent resolves the case without human intervention → Sierra gets paid a pre-negotiated rate

The case escalates to a human → Sierra gets nothing

“For a customer service context, that means if the AI agent resolves the case, no human intervention, there’s a pre-negotiated rate for that. If we do have to escalate to a person, that’s free. For sales, it would be a sales commission. Wherever possible, there’s a way to align our interests with our clients’, we choose it.”

The closest precedent for what Sierra is doing is the shift from impression-based ads to cost-per-click:

“I don’t think any ad platform thinks ‘man, think of all the impressions we’re giving away for free.’ When you charge for something closer to a business value, it’s actually more valuable. It’s more efficient.”

CPC took over because once one platform proved the alignment worked (Google), and Sierra is making the same bet on enterprise software.

Every incumbent in customer service software runs on per-seat subscription revenue (i.e. Salesforce Service Cloud, Zendesk, Intercom, etc).

But to match Sierra’s pricing model every one of them would have to cannibalise the revenue base their public market cap is priced on:

Business model transitions are harder than technology transitions. The revenue dips for a period as they come back out. And any public company CEO will tell you that's easier said than done.

Outcome pricing is the lever everyone sees, but the lever underneath it (the one that actually decides whether Sierra wins) is speed-to-live.