🌊 Higgsfield AI: $0 to $500M ARR in 15 months

The growth playbook behind AI video's loudest company

👋 I’m Ivan. I study how top 1% startups grow. Over 24,000 subscribers turn to us for growth strategy deep-dives. In case you missed it:

This newsletter is an educational resource (template to get it expensed)

Hello there!

This week we deep-dive into Higgsfield AI, the rising (and controversial) AI video tool that lets you pick a template and out comes a cinematic clip (without prompt eng).

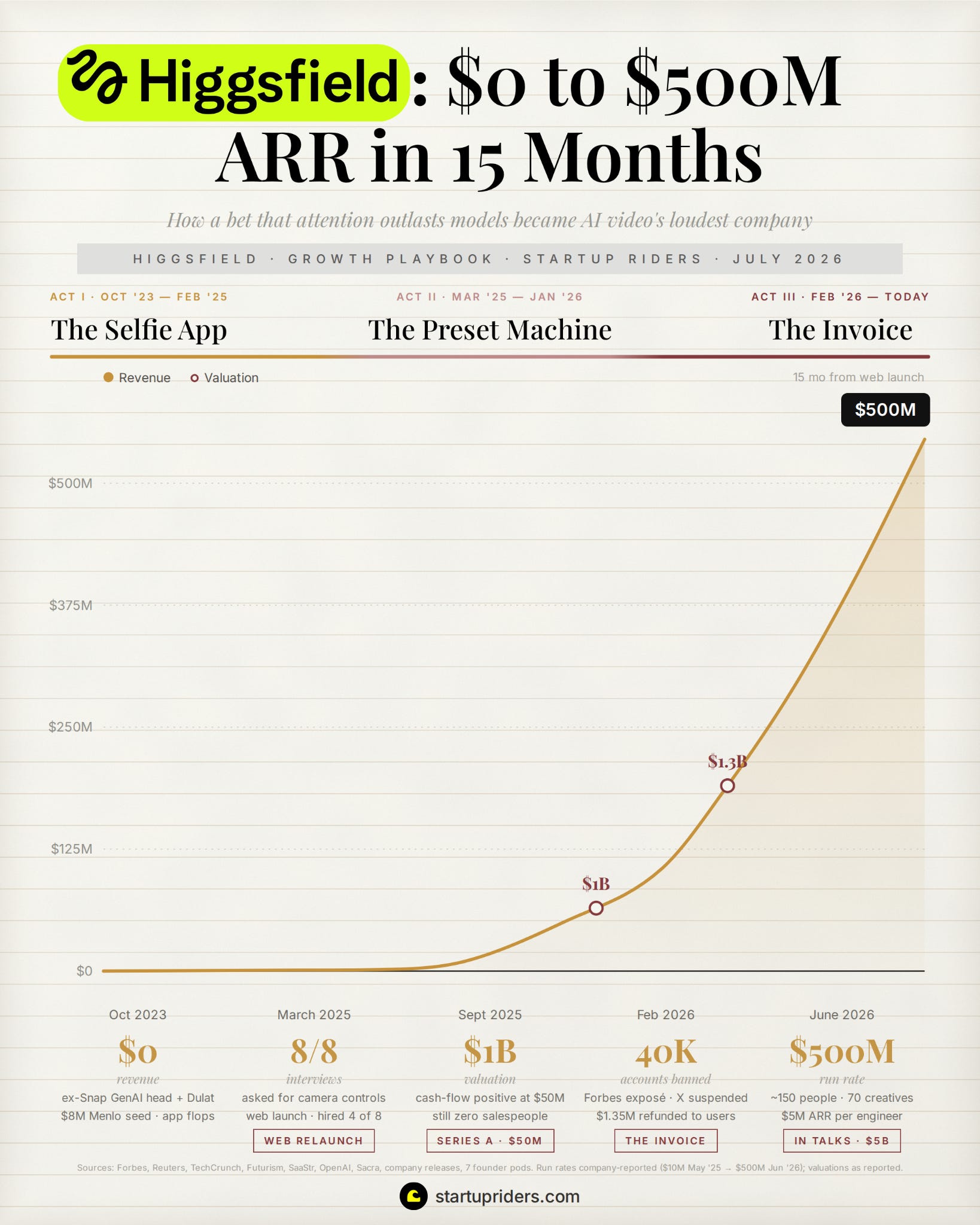

They launched the web product in March 2025 and 15 months later they’re at a $500M annualized run rate, apparently cash-flow positive, and supposedly in talks to raise at a $5B valuation.

In February Forbes published an investigation into how they grow (not flattering). The revenue curve is one of the fastest I’ve charted while the baggage is very real (there’s literally an entire site called higgsfieldsucks.com built by burned customers), so treat this as a deep dive into how the growth machine works, not an endorsement of everything they did to run it (we get into that in the cost of velocity section):

I dove into 7 founder and cofounder podcast transcripts, the Forbes investigation, Reuters and TechCrunch reporting, OpenAI’s own case study on them, and dozens other sources to figure out how they grew.

What you’ll learn

The interviews that produced their first product

How they got to $60M+ ARR without sales-people, and the distribution cascade they used (X to Instagram to Telegram)

Why 70% of revenue comes from the creative agencies they are disrupting

The pricing ladder that starts at $10/month and ends at 5x Canva’s ACV

How they turned virality into an engineering metric

The cost of velocity (the good, the bad, the ugly)

Lets dive in.

📐 Quick note on editorial and methodology: this is me surfacing the 80/20 anomalies that explain Higgsfield’s growth (not a comprehensive profile and not an endorsement or investment advice). Long-form founder interviews (SaaStr, Hockey Stick Growth, Deconstructed VC, etc) plus reporting from Forbes, Reuters, TechCrunch, Futurism, WSJ, etc. Company-reported figures are marked as such. Treat directional estimates as directional.

Act 1: The selfie app nobody would pay for

Alex Mashrabov’s mother designed rockets for the Soviet space program. He started programming at 10 and ranked among the world’s best competitive programmers at 20. He spent a year at Yandex training neural translation models that beat Google’s Russian-English system in 2014, back when, in his words, the whole idea “felt so outrageous and so romantic and so unpractical” that the team apparently hid their training runs from managers.

His first startup was a homework-solving app that lost to Photomath. His takeaway:

“That’s where I learned the first rule of venture. Winner takes it all.”

His second, AI Factory, sold to Snap for $166M in 2020 and became the tech behind Snapchat’s Cameos and face filters. He ran generative AI at Snap and collected 2 scars there:

Distribution scar: watched TikTok eat his employer where by late 2022 the average US teenager spent 90 minutes a day on TikTok against 27 on Snapchat.

Compute scar: ByteDance had “tens of thousands of H100s in GCP” before ChatGPT launched while Snap’s cloud was built for recommendations (vs generation).

The lesson he took was that distribution and compute decide these races and that incumbents can be asleep in one while dominant in the other.

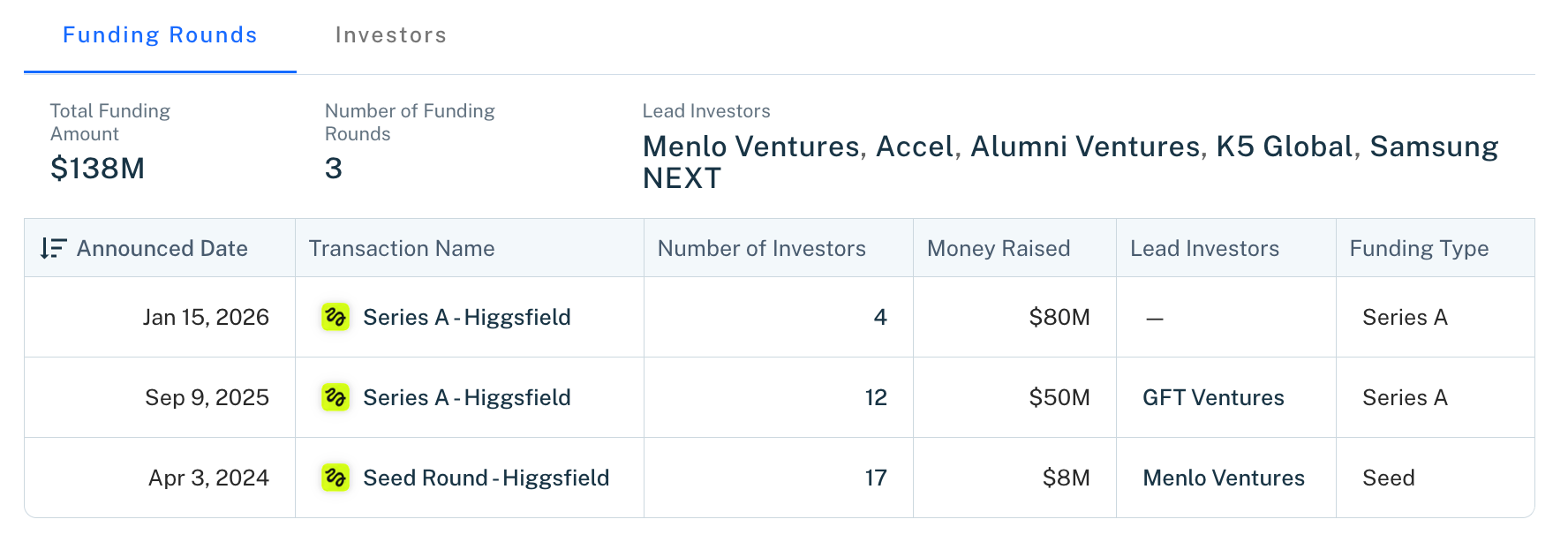

He left in September 2023, found Yerzat Dulat (a Kazakh researcher who trained diffusion models daily, which was Mashrabov’s filter for a cofounder), and raised an $8M seed from Menlo Ventures in April 2024.

The first product was Diffuse a mobile selfie-to-video app launched in India, South Africa, the Philippines, and Central Asia. It got users but did not get money.

“Generative AI doesn’t change the economics of mobile apps. High churn, small ticket sizes, limited expansion.” (Evolving Edge)

They burned most of the seed learning this, it was interesting to hear them on stage with Jason Lemkin 2 years later calling the consumer spend “tuition”.

The 0 → 1: how Higgsfield got its first customers

In early 2025, with the mobile app stalling, the team ran customer interviews with professional video people they had no relationship with (on purpose) to get unfiltered opinions. Apparently a mix of Hollywood-level movie directors down to regional producers of commercials.

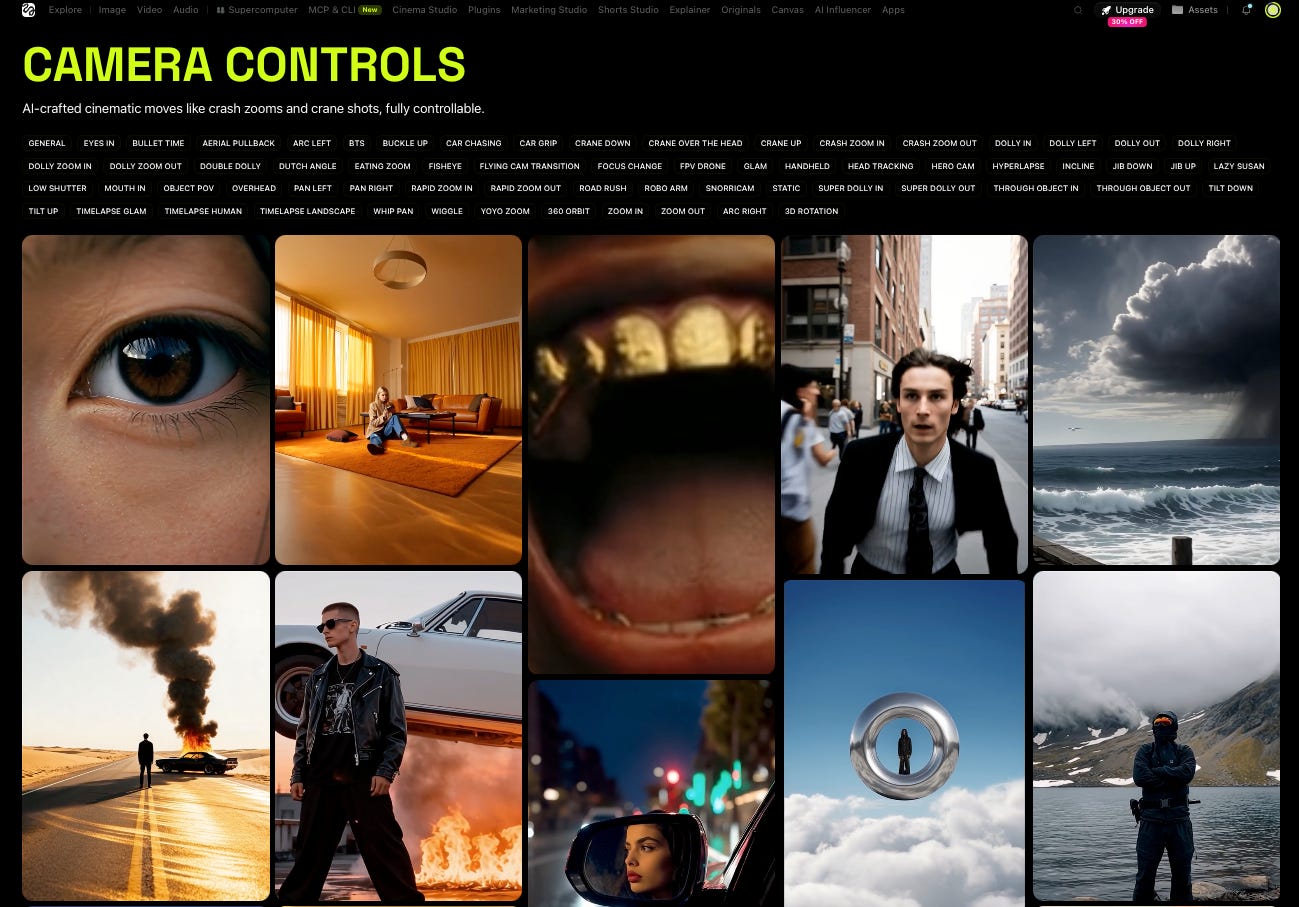

Creative directors were rejecting AI video because there was no intention behind the camera (i.e. no dolly-in, crash zoom, orbit etc). What they did:

Built exactly what 8/8 asked for: camera controls shipped with the web relaunch on March 31, 2025 (Mashrabov’s own date).

Hired 4 of the 8 interviewees: moved that feedback loop inside the company which ended up scaling to 80 engineers paired with roughly 70 working filmmakers, with tutorials and marketing assets they publish generated on their own platform: “The creatives tell the engineers where the models fall apart. The engineers fix it. That loop is the product.”

$10M ARR in under 2 months: Mashrabov has given both “five, six weeks” and “8 weeks or so” in the same interview, and his own LinkedIn telling dates the launch to April and the $10M to “the first month,” so I’ll stick with “under two.” A GFT Ventures partner told Reuters they had never seen anything like it.

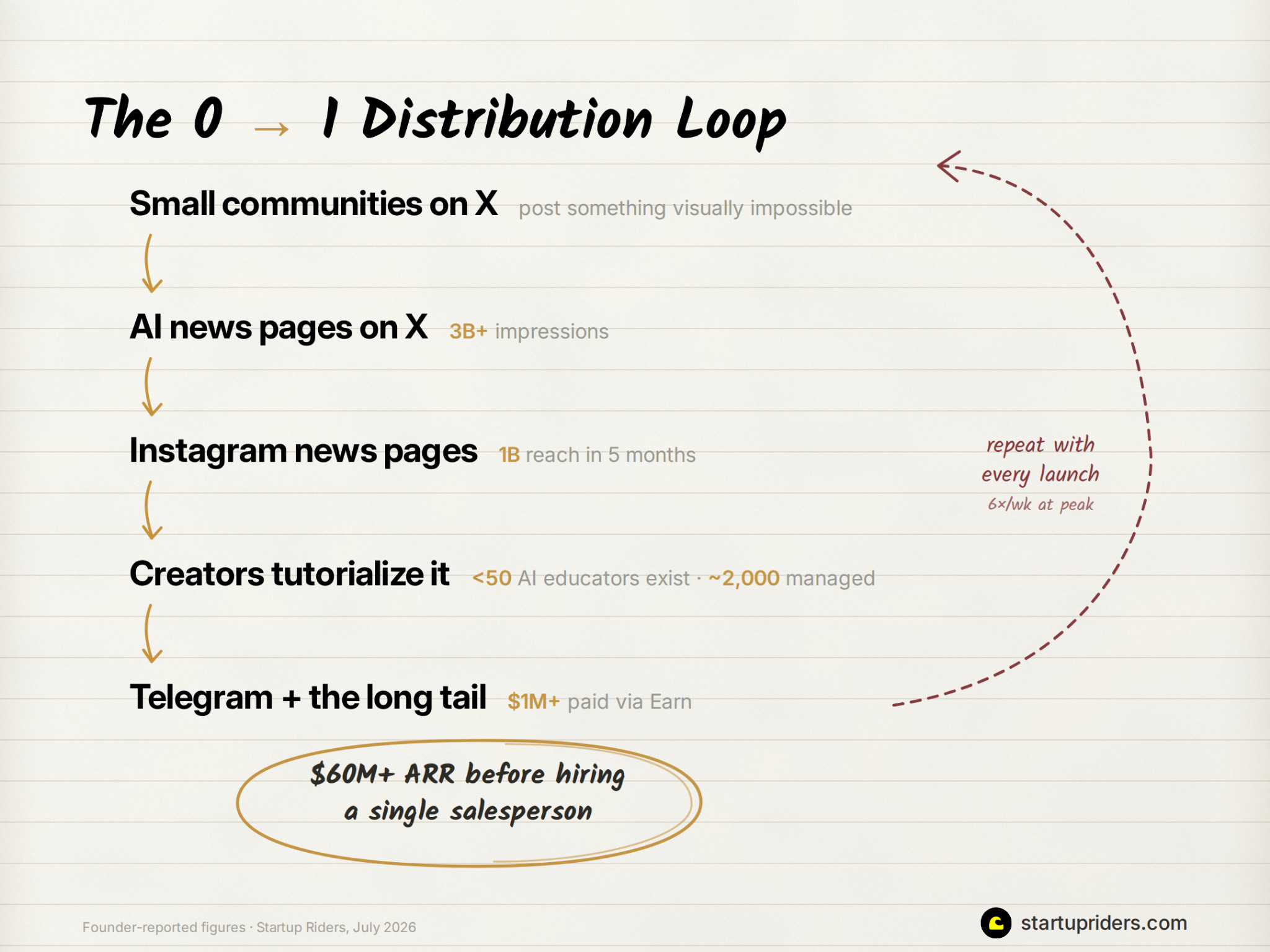

$60M+ ARR before the first salesperson: per cofounder Mahi de Silva: “60 plus million ARR without a single salesperson in the company.”

No salespeople does not mean no distribution thought it just means that the distribution was a cascade (as mapped by the founder):

Then they repeated with every feature launch, up to 6 a week or so.

Growth Lever 1: They sized the market by who wants the output (vs who can use the tool)

“We made a bet that the number of people who want to sell [on social media] is probably tens of millions of users. But the number of people who want to learn prompt engineering is probably hundreds of thousands. And there is this immersive gap which someone has to close.” (SaaStr)

Every AI video company in 2024 was building for people willing to learn prompting but these guys made the opposite bet:

Tens of millions of people need social video to sell something

Hundreds of thousands will ever learn to prompt

2 orders of magnitude sit in between and whoever closes the gap collects the difference

The output was 100+ cinematic templates + pre-set camera moves, mostly click-first vs prompting. De Silva marks it as a defining moment of the company:

“templates instead of a prompt box... it took off almost instantly.”

Mashrabov’s model rests on 1 asymmetry which is that video models commoditize (a new state-of-the-art one ships roughly weekly), but attention doesn’t, and as you’ll see below very growth lever is a machine for acquiring attention cheaper than rivals and converting it before the next model reset.

Growth Lever 2: They became the storefront for every rival's model

“Whenever a new state-of-the-art model dropped, we integrated it within 24 hours. Customers learned they could trust Higgsfield to always have the latest, best-performing AI.” (Evolving Edge)

Higgsfield launched on its own model and they called it “open source plus plus plus”, but then reality arrived:

“We realized very quickly that the number of models just increases, basically a new model coming every week... this is actually an opportunity for one platform to consolidate all the models.”

They rebuilt as the storefront on everyone else’s models, with these mechanics:

12+ models on the shelf: Veo, Kling, Seedance, WAN, plus their own remaining models, runnable side by side on the same prompt.

A 24-hour integration rule: customers stopped shopping around because the newest model was integrated fast.

An explicit lineage: on Deconstructed VC the host offered “it’s always good to be Switzerland. It worked well for Perplexity and Cursor,” and the founder confirmed: “we take a lot of inspiration from these 2 companies.”

“Contempt” for the alternative: Runway according to them is “incentivized to spend a couple hundred million dollars to catch up with Google and OpenAI in terms of pure model capabilities, which is a weird thing for a startup to do.”

And this growth lever has already been tested for real when a dependency risk popped up i.e. OpenAI discontinued Sora in the spring of 2026, and Higgsfield was apparently its second largest customer!

Act 2: The preset machine

By August 2025 they were cash-flow positive at $50M ARR and ran it to $200M and a $1.3B valuation over the next 5 months:

Growth Lever 3: They fired the customers who wouldn’t pay (on a ladder planned since 2024)

“We had to skate towards where people are willing to spend money. We don’t have the deep pockets of an OpenAI or an Anthropic.” (Mahi de Silva)

The mobile-to-web pivot gets told as a scramble but it was very intentional: