Most AI note-takers just transcribe and summarize. Granola is an AI notepad. You jot down what matters during the call, and Granola uses your notes plus the transcript to generate summaries, action items, and next steps from your point of view. The powerful part: you can chat with your notes. Write follow-up emails, pull out decisions, prep for your next meeting — all in seconds.

I don’t promote tools lightly. This one earned its place.

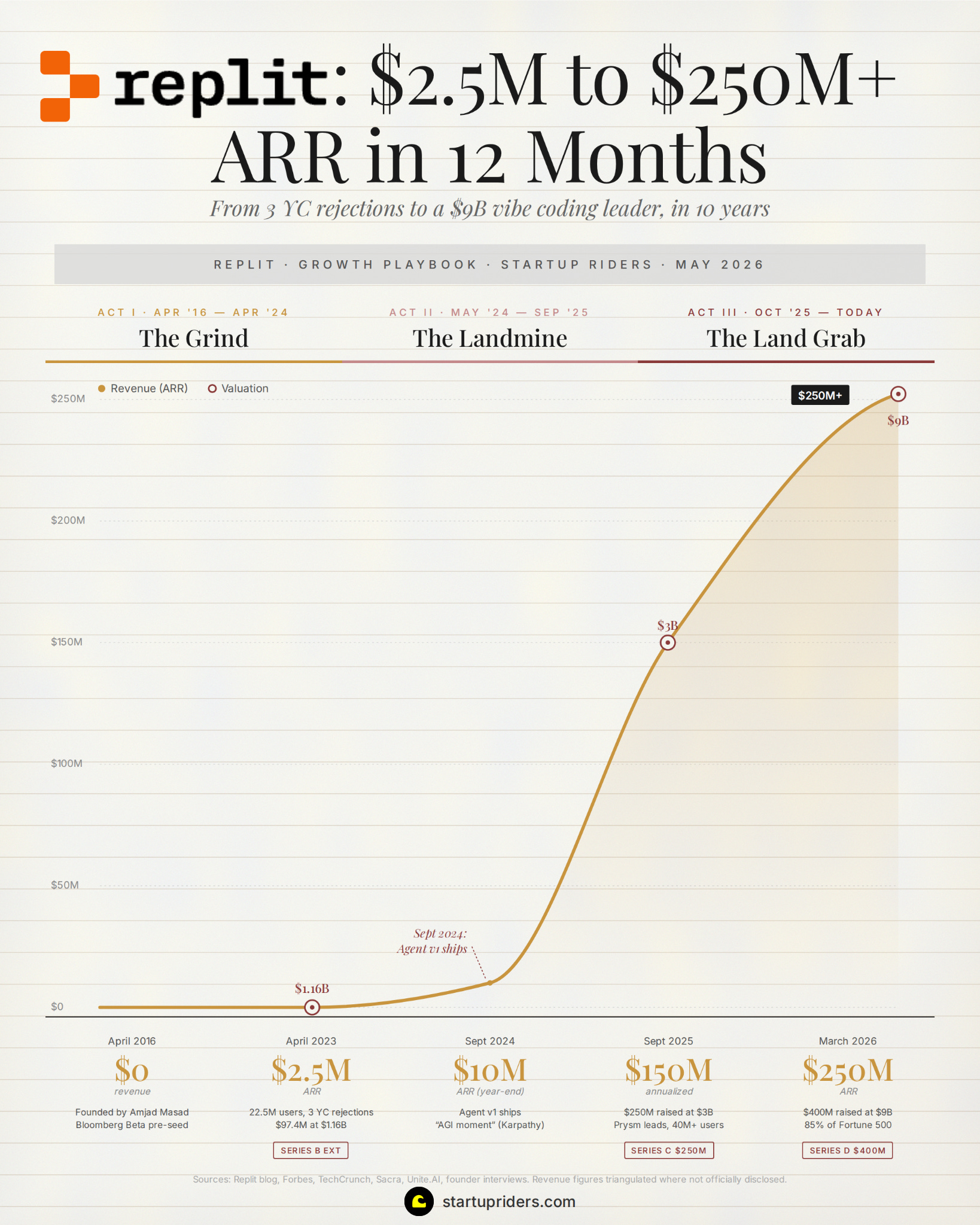

Every operator I know has now heard the story of Replit hitting $250M ARR last year but most have no idea what’s actually under the hood.

I’m excited about this one because I’ve been using Replit for a few years now, and always loved the product (i.e. built a Pitch Deck GPT to 50K+ conversations on OpenAI and used Replit to use it outside their wall-garden):

Their revenue and funding velocity has made them quite the outlier:

They call themselves the “agentic software creation platform”. I interpret as an ambition to own the whole stack from “type an idea” to “your app is live with users and revenue” with one AI agent driving it. We’ve covered Lovable’s growth curve before, but Replit’s Agent was the first breakthrough product of its kind, credit where credit is due.

So I spent the past week pulling apart 20+ founder interviews, every Replit blog post since 2018, every press release of their 8 funding rounds, and all customer case studies I could find.

What you’ll learn in this edition:

How Replit went from $2.8M to $250M ARR in 12 months

The Tesla-style master plan Amjad Masad wrote in 2015 (before ChatGPT)

The 6 months in 2024 when employees were quitting daily

The 10-person stealth team that built Replit Agent through the desert

The 1-week pivot that rebuilt every team for AI users instead of human ones

The pricing change that took ARR-per-employee to $2.5M

Why Anthropic, Google, and Microsoft ship Replit their newest models on day one

And as usual, a few growth lessons for you to steal at the bottom.

Let’s dive in:

📐 Quick note on editorial and methodology: this report is my best attempt at surfacing the 80/20 positive anomalies that explain their growth (my opinion, not a comprehensive company profile). Sourced from 20+ podcasts and long-form interviews with Masad and team (My First Million, Sequoia Training Data, Masters of Scale, 20VC, Lenny’s, YC, Joe Rogan, and others), plus reporting from Forbes, TechCrunch, Semafor, Bloomberg, Inc, Sacra, and Replit’s own blog. All revenue figures and funding rounds sourced. Treat directional estimates as directional.

Act 1: The Grind (April 2016 → April 2024)

Eight years, 3 YC rejections and 1 master plan.

In 2015, Amjad Masad sat down and wrote a 3-step plan for the company he hadn’t started yet. The deck looked a bit like Tesla’s master plan, bear in mind this is 2016:

Amjad quit Facebook in 2016 and co-founded Replit with his wife Haya Odeh and his brother Faris. The first investor was Roy Bahat at Bloomberg Beta, who Masad had met during his Codecademy days, on a ~$500K pre-seed round (with 100K monthly active users! let’s just say the fundraising environment is… different today).

By late 2017 they had 3 Y Combinator rejections and weren’t even getting invited to interviews. Then Sam Altman DM’d Masad on Twitter and said come meet me at OpenAI’s mission office. They talked, and Altman told him it was Paul Graham who’d actually found Replit on Hacker News, but PG was retired and living abroad, so they’d have to talk by email.

What followed was a 2-month email exchange between Masad and PG, during the holidays, that Masad later described as feeling like “talking to a prophet”. On the night before YC W18 was about to start, Sam told them to submit a late application “even if you don’t have time to answer all the questions” and that the interview would be the next morning. They got in + a $120K check.

By April 2023 they had raised $97.4M at $1.16B, with 22.5 million users, but “only” ~$2.8M ARR. A unicorn that wasn’t quite a unicorn just yet.

So, how did they get there?

Growth Lever 1: Picked the smallest possible buyer, in countries Silicon Valley wasn’t even pitching yet

Build for the future buyer, not the current one.

Replit’s Pre-Seed Deck

Most YC-backed dev tools target professional developers because that’s where the budget is but they ignored this and targeted 13-to-17-year-olds learning to code.

The economics were not ideal (school and education customers don’t tend to pay much), the procurement cycle is awful, and most of the users are minors who can’t transact.

Apparently every investor they pitched in 2016-2018 told him to go after pro devs for this reason, but just like we saw in the Granola growth playbook, outlier founders tend to dance to their own drumbeat, and Amjad fits in this bucket.

Their play was different (contrarian and right they say). The kid playing with Replit at 15 becomes the founder at 25 and the buyer at 30.

And, more importantly, kids in countries Silicon Valley doesn’t ship to could use Replit because nothing had to be installed (the product ran in a browser). Every laptop, including the second-hand Chromebook in a school in Lagos or Jakarta, suddenly had a full development environment in it.

“Originally the US was dominating by a lot. We see certain countries light up at the same time. The strongest growth right now is coming from more developing parts of the world. India is the strongest one, but we’re seeing really strong growth in the Middle East and Africa as well.”

By 2021 Replit was the dev tool of choice in India, Pakistan, the Middle East, and several African markets. While Cursor and Lovable hadn’t been founded, while GitHub was mostly invisible to anyone without a credit card, Replit had already built distribution into the markets every western tool wanted to be in 5 years later.

The product mechanics they shipped to make this work:

No-install dev environment, browser-based, runs in any tab. Crucial for users without GitHub-quality dev machines.

Multiplayer (2018), real-time collab on code, like Google Docs for programmers. Made pair-programming free across timezones.

Free tier with real compute. Half a virtual CPU and 500MB of memory free, forever (heavy enough to build with).

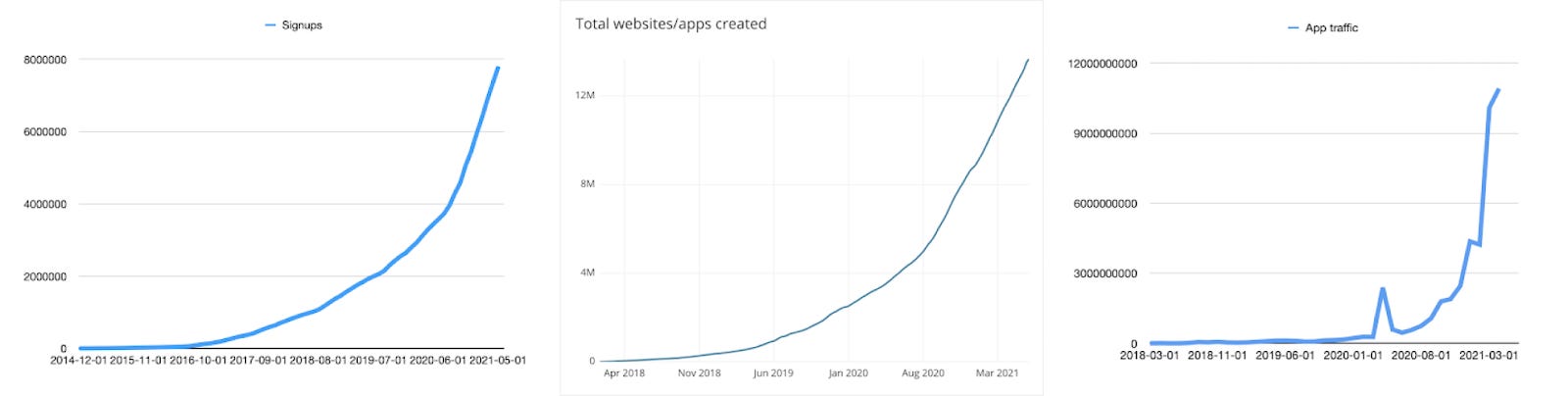

This added up to a 10-year cohort of users who became Replit-native before they were technical and by 2023, the platform had 22.5M registered users and you could see the geographic distribution in the user logos.

By the time the AI wave broke they didn’t need to acquire its non-technical buyer (PMs, designers, ops people, lawyers etc) because they were already kind of there.

Worth flagging here that this was the move competing tools structurally can’t copy because going after kids and emerging markets in 2017 looked like an obvious negative-NPV decision (you need 10+ year horizon).

Growth Lever 2: Made platform bets when everyone else made narrow bets

“We should be ambitious enough to support everything, not pick one lane and hope it wins.”

In 2016 most venture-backed dev tools were picking a single lane (i.e. Glitch bet on JavaScript, Cloud Nine on browser-based execution, etc).

The founder made 3 bets in the opposite direction:

Multi-language from day one: Python, Ruby, C, Java, Go, Rust. Glitch’s seed round was many times Replit’s pre-seed (they’d raised a 30M Series A).

Cloud over browser: The original Repl.it ran code inside the browser tab and that “capped” what users could build. So they moved execution to containers on real servers and kept the interface in the browser (not an easy trade-off).

Open it in the browser, not as an app you install: Every other IDE (the software developers use to write code) in 2016 was a desktop app but Replit worked like Figma or Google Docs (open link, share it, 2 people in the same project at once). Figma had proved the model for designers but nobody had built it for coders.

Remember Step 2 of the 2016 master plan (the AI layer)?

The founders treated it as a real product layer from 2017. They’d built 1 throwaway ML feature every year and apparently killed each one before it shipped because pre-transformer models couldn’t compile code or hold context past a few lines.

They built it anyway because the point was keeping a small group close enough to the research that when something crossed the “usefulness threshold” they’d immediately recognize it and jump on it.

That moment came in February 2019 when GPT-2 dropped, and they shipped:

June 2020, Explain Code: Replit got into OpenAI’s GPT-3 private beta (a small group with early access) and shipped a feature that let developers highlight any code and get a plain-English explanation. One of the first real GPT-3 products in market where each query cost more than they charged the user (ran it anyway).

June 2022, Ghostwriter: Microsoft had locked up GPT-3 with an exclusive license in late 2020 blocking everyone else, so Replit trained their own AI on top of a free model from Salesforce and shipped Ghostwriter (AI that writes code as you type) 3 months before GitHub Copilot was public.

May 2023, their own model: Michele Catasta, who ran Google’s PaLM AI team, quit after Google refused to ship a code version. He joined as VP of AI and 3 months later a team of ~30 engineers trained Replit’s own AI and beat every free model in the world at writing code.

What that bought them by April 2023:

More AI features in production than any developer tool company.

Internal tooling, evaluation infrastructure, and fine-tuning workflows battle tested.

Day-one access to new models from every major lab.

The Series B Extension closed in April 2023 at $1.16B with a16z Growth leading (2.8M ARR…).

Replit Series B deck

Act 2: The Landmine (May 2024 → Sept. 2024)

The desert

By early 2024 Replit had ~$2.8M ARR and were likely burning through a lot of cash (thesis hadn’t yet converted into revenue).

Then the AI wave broke and the company was caught (a little?) flat-footed:

Cursor launched in March 2023 and was growing faster than anyone.

v0, Bolt, and every week another AI coding product launched on Twitter.

A few specific things broke at once that hurt them:

Pro devs wouldn’t pay: they’d spent 2 years building features for professional devs (advanced deployments, team collab, custom domains) but pro devs looked at Cursor and bought Cursor.

Education revenue capped out: Teachers and schools were the original buyer but as we talked about earlier this is a tough market (unit economics never funded the AI infrastructure spend).

Free tier got expensive: ~30M users were running compute on their infra for free and per-user cost went up every time the team shipped a new AI feature.

Investor patience was thin: Cursor raised at $400M in October 2023 with better revenue than Replit had at $1.16B (a16z were in both for example).

I heard Amjad talk about this part of the story and credit to him for opening up about a part of startup life that is not often talked about and yet very common. The team started leaving and it was a very hard moment for them, he described it as watching the company bleed out one Slack departure at a time.

Worth flagging that the trap wasn’t a bad product (the product was amazing), but that the user Replit had built for (the professional developer) was getting eaten by Cursor faster than Replit could compete, and the user Replit could win (the non-technical builder) didn’t yet exist as a category anyone paid for.

In May 2024 they made a series of moves (some very hard):

Cut the team to ~30 people: Engineers, designers, support, founding-era hires.

Pulled 10 engineers into a stealth team: with an assignment to rebuild the editor, runtime, and deploy stack for an AI agent.

Gave them 90 days: The rest of the company kept the existing product running.

Bet on Claude over their own model: Reversed the 2022-2023 “own the model” strategy and built an Agent on top of Anthropic instead of fine-tuning internally.

Threw out every pro-dev feature: Team collab, advanced deployments, custom domains etc.

By August they soft-launched the way game studios do to PMs at portfolio companies, designers at YC startups, solo founders Masad knew etc, and the success rate was high enough to commit to a September public launch.

Agent v1 ships

Agent v1 went live and in the first 7 days:

Day 1 = $1M in new ARR: More than any single month of the prior 18.

Day 2 = $2M: ARR line went near-vertical.

Week 1 = ~$10M ARR added: More than the entire base built in 8 years.

500K+ apps built: Most by non-technical users.

By December they were at $50M ARR, by September 2025 they raised the Series C at $3B on $150M ARR and by March 2026, the Series D at $9B on $250M ARR.

Act 3: The Land Grab (Oct 2024 → today)

Growth Lever 4: Rebuilt every team for AI users instead of human ones

“The org chart for a developer tool company and the org chart for an AI agent company are not the same company. We rebuilt around the new user in a week.”

In the week after launch they had to rebuild every team:

Killed the enterprise sales pipeline: Cut outbound to Fortune 500 CTOs and redirected the reps to inbound from PMs, designers, and ops people already building on Agent.

Rebuilt support around non-technical tickets: new team was generalists handling “what is a database” and “how do I share my app with my boss.”

Reshot the marketing site in 5 days: the new homepage was the same one-button entry as the product: “what do you want to build today?” which apparently led to signup conversion going from low single digits to 12%+.

Renamed every product surface in plain English: “Repls” became “Apps.” “Deployments” became “Publish.” “Environment variables” became “Secrets.”

Built a new growth team from scratch: Hired 4 generalists from consumer software companies. New mandate was acquisition through consumer channels (Twitter, TikTok, LinkedIn, creator partnerships).

The compounding effect:

Activation rate (signup → first deployed app) roughly tripled in 90 days.

ARR-per-employee went from ~$50K to over $2.5M within a year.

Growth Lever 5: Publicly pointed their biggest user segment at the competitor

"We don't care about professional coders anymore."

By late 2024 professional developers were a large share of Replit’s usage and a small share of revenue, but the non-technical builder was converting at a higher rate.

They spent late 2024 and early 2025 publicly drawing the line that Replit was for non-developers and that the company had stopped competing for the professional developer market.

Why the public handoff worked vs a “typical” quiet deprioritization:

Cleared the roadmap publicly: Team had air cover to kill every pro-dev feature on the backlog = no internal debate about whether to keep building = speed.

Hard-positioned out of the dev tools category: Market stopped comparing them to tools built for engineers, they competed in the non-technical wedge.

Surfaced the right ICP faster: Made it easier for non-technical buyers to self-identify and convert (pipeline velocity).

Made the next pricing change defensible: When they repriced the non-technical tier (Lever 6 below) nobody was confused about who it was for.

Next, they pulled on a lever that got them to 80-90% enterprise margins while most AI coding companies were still unprofitable.