Attio is the CRM that transforms how top teams grow. Ask Attio how to win this deal, what to say in your follow-up, where your pipeline actually stands, and get answers with full context, instantly. With Universal Context, Attio’s intelligence layer, every signal across your tools becomes instantly actionable. The engine behind every top 1% startup is a great CRM.

Harvey AI’s Growth Playbook: Putting a lawyer in everyone’s pocket.

Hello there!

This week we’re deep diving into the growth playbook of one of the most important companies of this AI wave, Harvey.

This is a perfect storm story where you have a combination of extreme product-market fit (LLM’s usefulness on expensive, previously time-intensive, heavily text-based work), talent and investor hunger.

Attached was a proof of concept where they’d pulled 100 questions from r/legaladvice (reddit), ran them through GPT-3’s API using chain-of-thought prompting before anyone was talking about chain-of-thought, and sent the outputs to practicing landlord-tenant attorneys. Turns out 86 out of 100 answers passed and nobody at OpenAI had tested this.

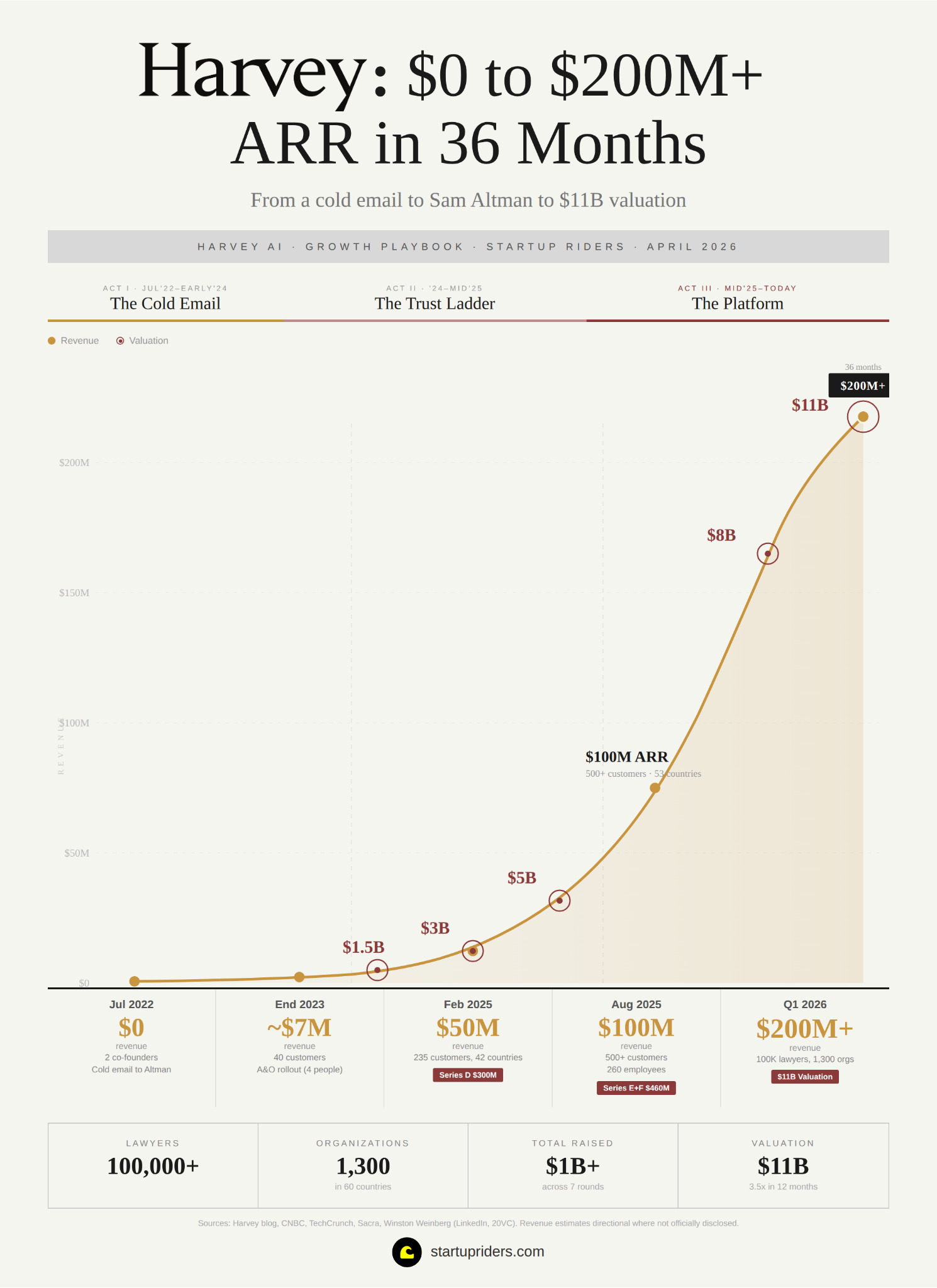

That email led to a July 4th pitch to OpenAI’s C-suite, a seed investment, and what became Harvey, going from $0 to $200M+ ARR in 36 months and an $11B valuation.

Two frameworks run through the whole story:

The first is prestige-led distribution: turns out that in professional services trust IS the product. Their hypothesis was that if you win the top firms first, even though it might be much harder to wedge yourself in initially, once you are embedded into those logos trust cascades downward through the entire industry.

The second is “expand and collapse”: Build specialized AI agents for narrow legal workflows. Then collapse them back into one interface that routes users intelligently. Which has become somewhat of a blueprint or operating system for how to build a compound vertical AI company in 2026.

What you’ll learn in this edition:

How Harvey went from a cold email to $200M+ ARR in 36 months with ~460 employees

Why they targeted the hardest law firms first when every VC said start small

The “expand and collapse” product strategy that is the actual playbook for vertical AI

Why Harvey’s CEO says GRR is the metric most AI investors are dangerously ignoring

How they’re shifting from selling software seats to selling legal work through revenue-share deals

📐 Quick note on methodology: 7 podcasts (20VC, Sequoia, Greylock, Kleiner Perkins, Biography Pod, This Week in Startups, Upstart Media), plus press from CNBC, TechCrunch, Bloomberg, Reuters, Sacra research, and Harvey’s own blog. All revenue figures sourced. Treat directional estimates as directional.

Act I: The Cold Email (July 2022 to Early 2024)

How it started

Winston was a first-year litigation associate at O’Melveny & Myers in Los Angeles and his cofounder and roommate Gabe had spent a couple years doing AI research at DeepMind and Meta.

Gabe had been brainstorming horizontal AI assistant ideas with friends from Google Brain, who ended up joining OpenAI and building ChatGPT.

But he went in a different direction.

“Winston showed me all his legal tech. Their document search to search maybe 10,000 documents would take 5 to 10 minutes. He was like, I do the search and then I go on Instagram for a bit. The client gets billed for this.”

Everything in law was text, the workflows were deeply manual and the economics were, as we all known too well when we’re billed for a couple hours of legal work, big.

How the legal market actually works

To understand Harvey’s growth, you have to understand the industry.

The global legal services market is roughly $900 billion (and that is the size of the market today, lets not fall into the classic market sizing trap).

The average US lawyer bills $352 per hour, and the top partners at elite firms bill $2,000+. The gap between a junior associate and the best partner on earth is only about 3-4x in price, which Winston thinks makes no sense and will change.

Law firms are organized around billable hours. Partners give tasks to associates, associates bill hours, and the firm collects. Typically a junior associate does the first draft, a second-year reviews it, a fifth-year reviews that, the partner reviews it one final time, and then it goes out.

This hierarchy matters for AI adoption because it means there’s a built-in human-in-the-loop review system. The minimum viable quality of an AI output can be lower for a law firm than for an in-house team, because everything gets reviewed anyway.

What excites me the most about this tech shift’s impact on Legal work is that the average price used to put legal services out of reach for most people, until now.

But the path runs through the premium market first:

Instead they went straight to Allen & Overy (now A&O Shearman), one of the world’s largest law firms and signed a 4,000-person enterprise rollout.

At that time Harvey had 4 people and were working out of an Airbnb.

“Some of our investors were like, this is a horrible idea. Don’t do this.”

But Winston understood something about professional services that pure technologists usually miss, which probably came from having worked and experienced how a law firm did things first hand.

“If you earn the trust of a few of those firms, the rest of them will trust you and the rest of the firms downstream will definitely trust you.

And their clients will trust you.”

The logic was both GTM and product:

On the GTM side, prestige in professional services functions like a trust certificate. If A&O trusts you with their client work, every mid-market firm will trust you too.

On the product side, the hardest work builds the most defensible systems. If you can handle a $68 billion Activision-Microsoft merger, an NDA review should be trivial. ChatGPT could already handle simple NDAs, and going down-market first means building something the models will eat in 18 months.

“The thing that makes me feel better is if you get to the point where GPT-7 can just do a simple lease analysis... yeah, we’re probably done. But I’d also say pretty much every other company on earth is done.”

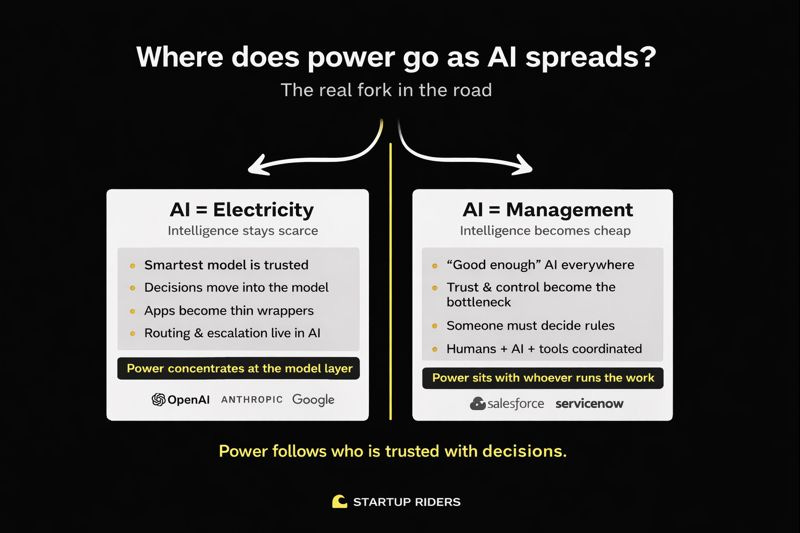

The bet Harvey took here is that intelligence will become cheaper and cheaper.

And if that happens:

“good enough” AI is everywhere

the bottleneck is no longer having intelligence

The hard problems become:

who is allowed to decide

under which rules

with which approvals

and who is accountable when something breaks

Which are coordination problems, not intelligence problems. You can think of coordination as deciding who does what, in what order, under which rules, and who is responsible if it goes wrong. The intelligence is not choosing the goal but rather helping move work through a system of approvals, handoffs, and constraints without humans chasing each other. In this world:

power shifts to systems that control workflows, rules, and decisions

intelligence is a commodity

whoever runs the work wins

This is similar to how Salesforce didn’t win by building better databases but by deciding how sales teams track leads, approve deals, forecast revenue, etc.

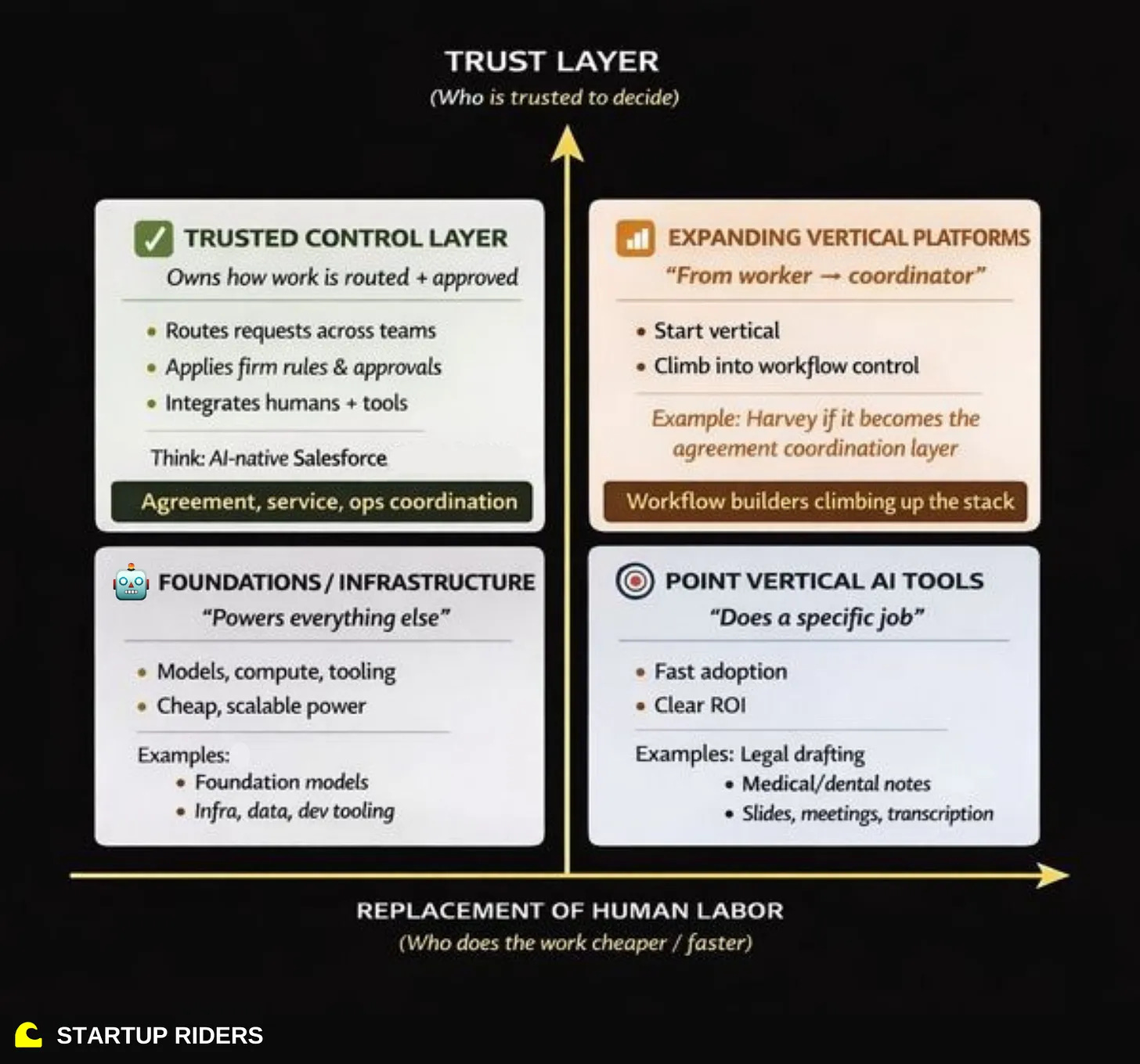

Harvey would have started as a Vertical AI tool, and if I’m right would be expanding to become a workflow builder climbing up the stack (platform).

Growth lever 2: Hyper-personalized demos that don’t scale

Before every pitch, Winston would look up the partner he was presenting to. He’d find a recent case they’d worked on (public court filings, merger agreements filed on EDGAR), and have Harvey analyze their own work.

For litigators apparently this move was pretty shocking.

He’d upload one of their own filed arguments and say:

“Tell me, make holes in these arguments. How would you argue against it? Lawyers are argumentative. Just let them fight with the model. They pay attention to every single word.”

Sometimes the model was wrong, especially in 2023 with early GPT-4, but that almost didn’t matter because the lawyers were reading every word, which no software demo had achieved before.

I’ve spoken on here before about talking to a lawyer friend of mine about using Harvey at work (before really knowing much about the company) and was shocked about how much value it drove for her (sharing the tool among multiple lawyers with one licence, saying it’d be incredibly painful to loose it).

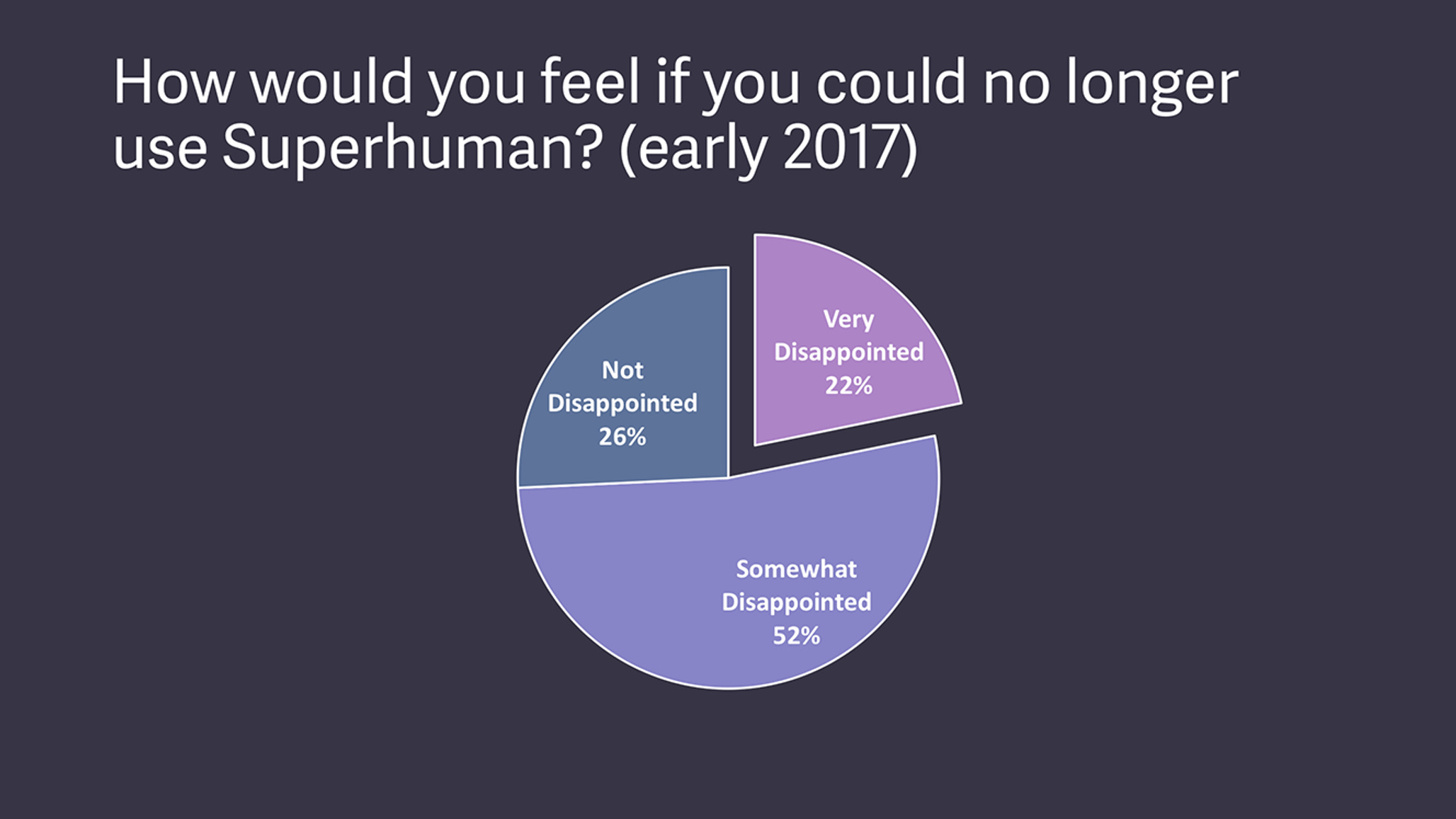

Reminded me of Superhuman’s product-market fit engine and its core question:

“A lot of these products, it’s just populating text and how do you get someone to pay attention to that? Well, you tell a litigator that there might be holes in this argument and they go... but they want to prove you wrong.

And so they really pay attention.”

This is gold for a sales team.

They’ve since productized this approach, where partners can now click one button and run their own matter through specialized workflows without prompting. Which means the thing that didn’t scale became a deployment strategy, and when partners share those workflows with their clients, it becomes distribution.

Growth lever 3: The trust flywheel (external virality)

Our strongest product-led growth has been external virality.

Harvey’s strongest growth loop is likely external, where law firms are bringing Harvey to their clients. Here’s how it works:

A private equity fund’s law firm builds a fund formation workflow on Harvey.

The firm shows it to the PE fund.

The PE fund says “we want this too.”

The PE fund is a happy customer, they start pulling in their other law firms.

A&O hit 70-80% daily usage during the initial pilot, so during the trial 3,500 lawyers asked 40,000 questions before the firm committed to a broader rollout.

Their first 50 enterprise customers were all referrals from law firm clients. By end of 2023, they had ~40 customers and were running at roughly $7M ARR (my estimate based on reported 4x growth to $50M by early 2025).

Act II: The Trust Ladder (2024 to Mid 2025)

This is where most AI companies stall or what we’ve been calling “vibe-revenue”. Now you have to actually retain, expand and build the machine that scales.

So how did they do it?

Growth lever 4: Expand the product, collapse the UI

| SwipeFile")