🌊 AI's $1T blind spot

Sequoia's new thesis, Anthropic's labour data, and 198 YC startups point to the same gap.

👋 I’m Ivan. I study how top 1% startups grow.

This week’s sponsor is AI CRM Attio!

Attio is the AI CRM for modern go-to-market teams. Attio connects to your email, calendar, calls, product data, billing data and more — so your CRM is always complete, always enriched, always in sync.

Prep for any call in seconds with full context across your business

Instantly prospect and route leads with research agents

Build powerful AI automations for your most complex workflows

Hello there!

This week I’ve been thinking a lot about one question:

Where is the next AI startup opportunity pocket moving?

3 things landed in my inbox that, once your layer them on top of each-other, tell a pretty compelling answer to that question (or at least a thesis). Today’s tl;dr:

🤖 Where AI works today.

🟧 Where 198 YC founders placed bets.

📈 The $1T+ in services TAM almost nobody is touching (yet).

📐 Quick note on methodology: AI coverage data comes from Anthropic’s Economic Index (one model’s usage, not all AI). Employment data from BLS (2024). YC sector mapping is my own analysis. Services TAM from Sequoia. Treat all numbers as directional.

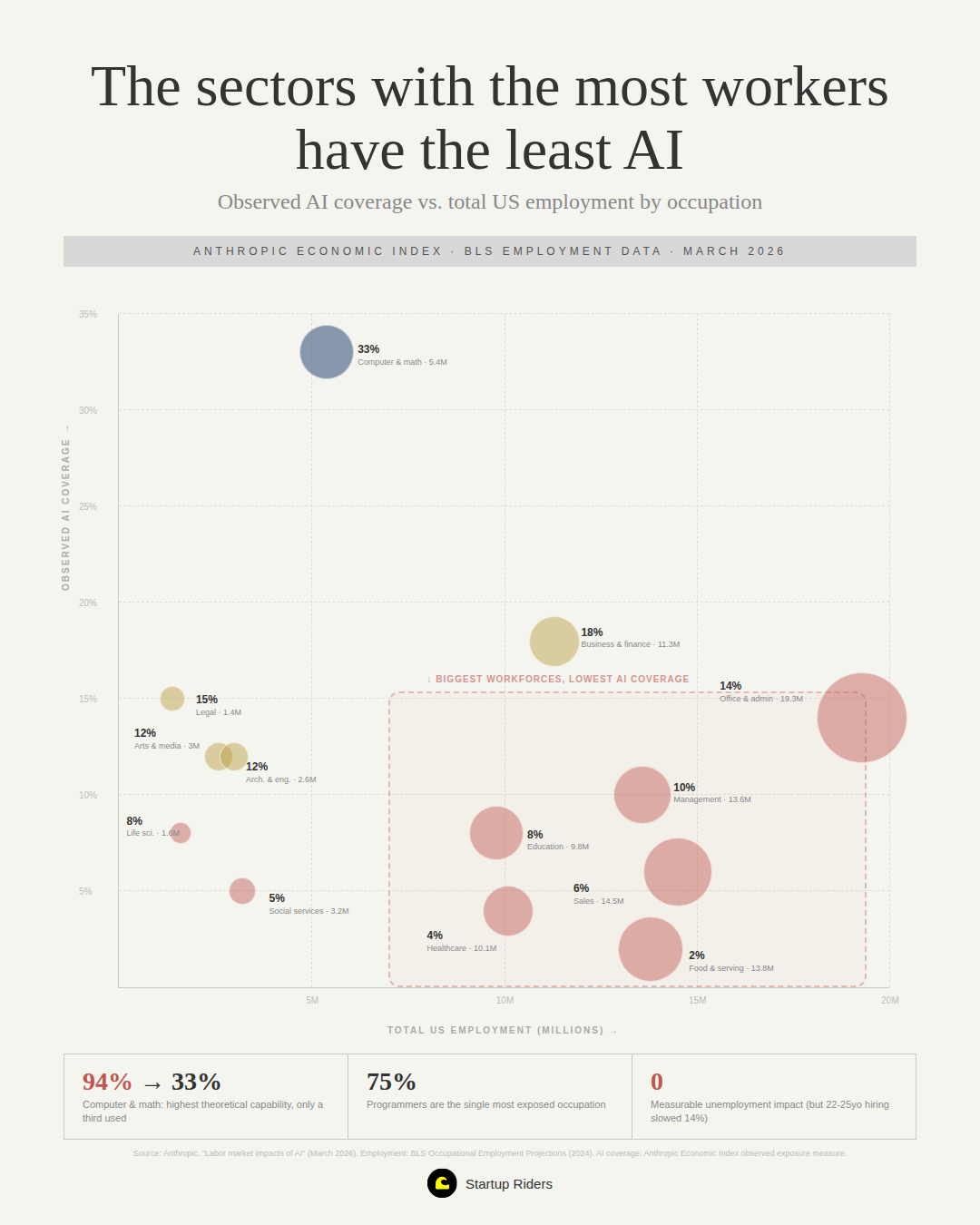

1. We’re barely scratching the surface.

AI is shockingly good at some tasks and pretty bad at others, but the boundary is unpredictable and moving fast.

The details

Anthropic dropped a new measure called “observed exposure” that combines what AI could theoretically do with what it’s actually doing today in the real world.

The numbers that jumped out:

Computer & math occupations: AI could theoretically cover 94% of tasks. But the actual coverage today is 33% (although moving fast).

Computer programmers are the single most exposed occupation at 75% coverage, followed by customer service reps (70%) and data entry keyers (67%).

Office & admin is 90% theoretically feasible but only 14% observed. Business & finance is 87% possible, 18% real.

Everything below that, education, healthcare, social services, construction, is in single digits.

This is what Alvaro (CEO of Luzia, 65M users) called the jagged frontier, where AI is shockingly good at some tasks and pretty bad at others, but the boundary is unpredictable and moving fast:

So what

The playbook that worked for code is likely coming to every profession where the work is more “intelligence” (rules, patterns, process) than “judgement” (taste, experience, context), more on that in a moment.

The bottom line for me here is that even though we have yet to find any measurable increase in unemployment for exposed workers since 2022, young workers are starting to feel the pain. Hiring for 22-25 year olds has slowed 14% in exposed occupations, which means that entry points to the labour market are narrowing, and we should be thinking more deeply about:

How do we get ahead of this trend, which is likely to accelerate.

Education reform (would love to see more startups working on this problem).

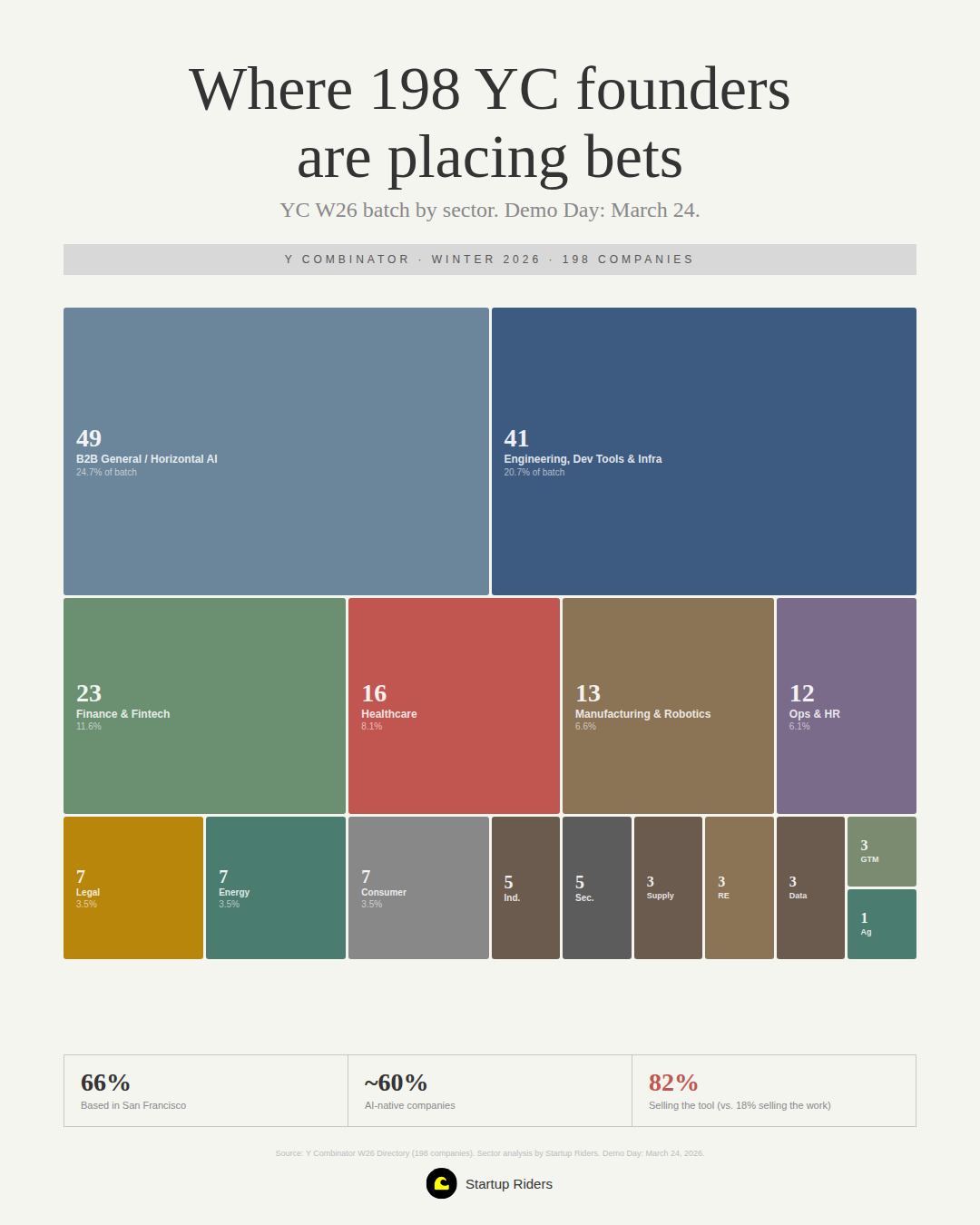

2. Where 198 YC founders are placing bets

82% of the batch is selling the tool. 18% is selling the work.

The details

This YC’s W26 batch is the largest yet with 198 companies. Here’s how they break down:

Engineering, dev tools & infra: 41 companies (21%). The most crowded single category. This is where AI adoption is already highest (per Anthropic’s data), and where the most founders are piling in.

B2B horizontal / uncategorized: 49 (25%). A grab bag, but many of these are AI wrappers, workflow tools, and agent scaffolding.

Finance & fintech: 23 (12%). Accounting, payments, lending, insurance.

Healthcare: 16 (8%). Drug discovery, healthcare IT, and a handful doing actual patient-facing work.

Legal: 7 (3.5%). Small but punching above its weight given Harvey and Legora just hit unicorn status.

So what

The batch confirms what Anthropic’s data shows which is that founders are building where AI already works, which is totally rational because the near-term PMF is obvious in software, finance, and legal (crossed the adoption threshold).

But it also means 198 of the smartest founders in tech are mostly fighting over the same territory, and this is an opportunity for you. The sectors where AI’s theoretical capability is high but actual usage is low (education, healthcare operations, social services, office admin) are almost empty.

Which brings us to the gap.

3. The $1T blind spot.

For every $1 spent on software, $6 is spent on services.