🌊 The 3 charts that explain the AI race

Ramp data, $19B run rates, and the metric nobody is watching

👋 I’m Ivan. I study how top 1% startups raise and grow.

This week’s sponsor is AI CRM Attio!

Attio is the AI CRM for modern go-to-market teams. Attio connects to your email, calendar, calls, product data, billing data and more — so your CRM is always complete, always enriched, always in sync.

Prep for any call in seconds with full context across your business

Instantly prospect and route leads with research agents

Build powerful AI automations for your most complex workflows

Hello there!

This has been another week filled with OpenAI drama.

And following the news of a 295% uninstall spike after they swooped-in to fill Anthropic’s U.S. Department of War deal, it prompted me to ask:

Who is actually winning the AI race?

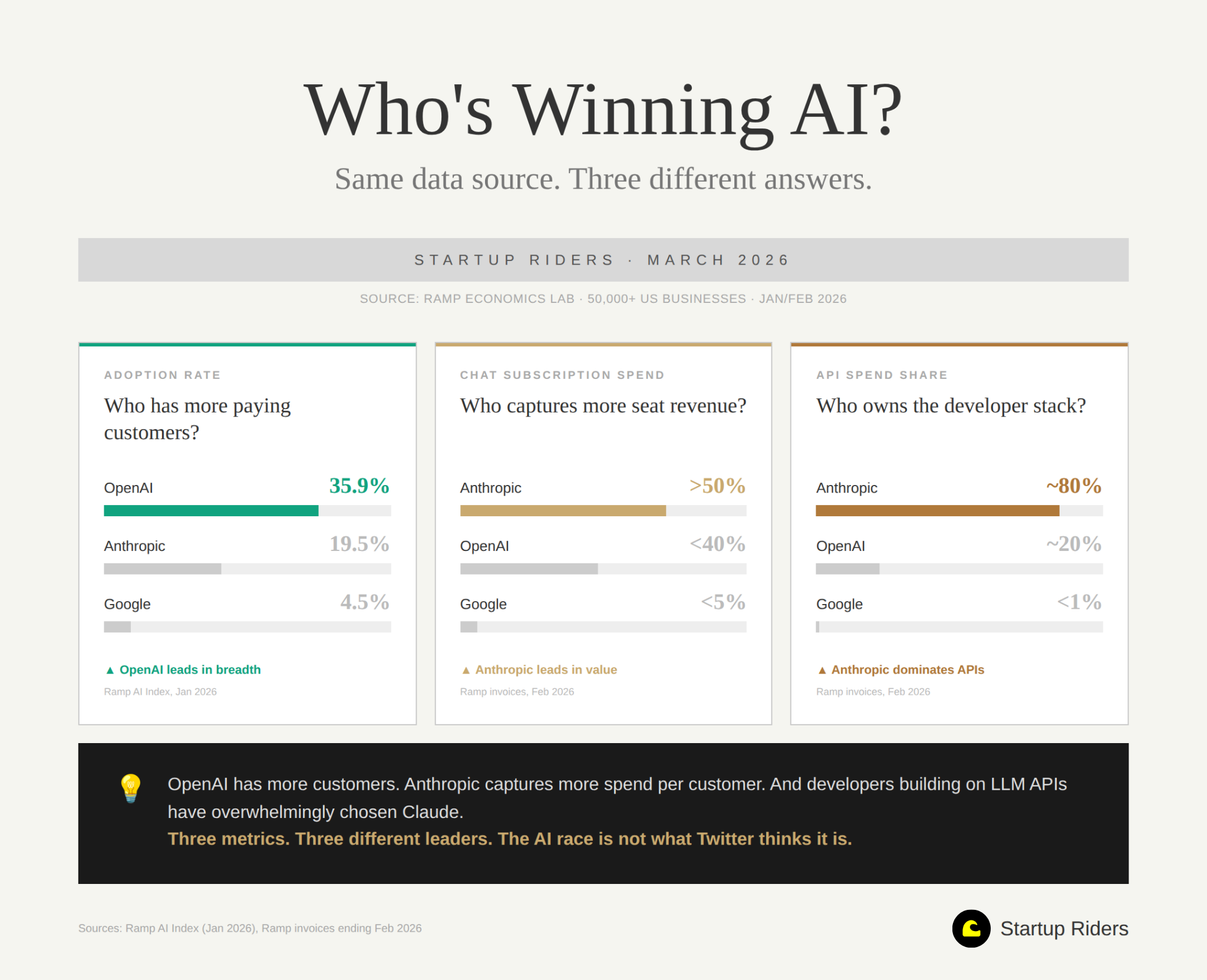

Ramp’s latest AI Index data came in handy to showcase a few insights on this following a couple viral tweets on the topic. One claimed Claude hit ~70% market share while another said OpenAI still dominates, and both cited the same data source.

Both were kind of right, but also both kind of wrong.

Today’s tl;dr:

🏁 Who’s winning the AI race (it depends which chart you read).

📚 Top 10 research reports this week.

🌊 43 European startups that raised €10M+ in February.

📐 Quick note on methodology: Ramp tracks 50K+ US businesses via corporate card and bill pay. It skews US, mid-market, tech-forward. The index measures three things separately (adoption, chat spend, API spend) and most viral takes conflated them into one “market share” number. Treat all numbers as directional.

1. OpenAI leads adoption (36%) but Anthropic leads spend (>50% chat, ~80% API).

Everyone is sharing the same data and reaching opposite conclusions.

The details

Ramp’s latest drop tracks 3 different things, and people keep confusing them:

Adoption rate (who has more paying customers): OpenAI leads at 35.9% of businesses vs Anthropic at 19.5%. Google trails at 4.5%.

Chat subscription spend (where seat revenue goes): Anthropic leads with >50% of enterprise AI chat spend. Claude Team, Max, and Enterprise seats cost more than ChatGPT Plus.

API spend (what developers build on): Anthropic dominates at ~80%. In July 2025, OpenAI had ~95% of this market. Eight months later, it completely flipped!! Claude 4.5 Sonnet and Opus have eaten the developer stack. There’s a fantastic interview on Lenny Rachitsky ‘s podcast with Claude Code’s creator well worth your time.

So what

OpenAI wins breadth, Anthropic wins value and the developer API market has picked a side (and if you have been playing with Opus 4.6 you probably have experienced why). The race looks very different depending on which metric you read, which is why “who’s winning” is kind of the wrong question altogether, but still fun to explore.

2. 16% of US businesses now pay for both ChatGPT and Claude. Double from a year ago.

The overlap is the metric nobody is watching.

The details

This is what I think is the most interesting number in the whole Ramp report:

79% of businesses paying for Anthropic also pay for OpenAI.

Churn rates are nearly identical at ~4% per month for both. If businesses were replacing one with the other, you’d see it in cancellations, but you don’t (so far).

The share of businesses paying for both doubled from 8% to 16% in 12 months

Anthropic went from 1 in 25 to 1 in 5 businesses in a year (4x growth) while OpenAI stayed roughly flat around 36%.

Total AI adoption hit 46.8%, an all-time high. Nearly half of US businesses now pay for AI, whereas two years ago this was close to zero.

So what

Businesses are actually stacking providers, where different teams with different use cases at same company use different models at different times. If you’re building, designing for a multi-model world likely makes sense since customers seem to already be doing it.

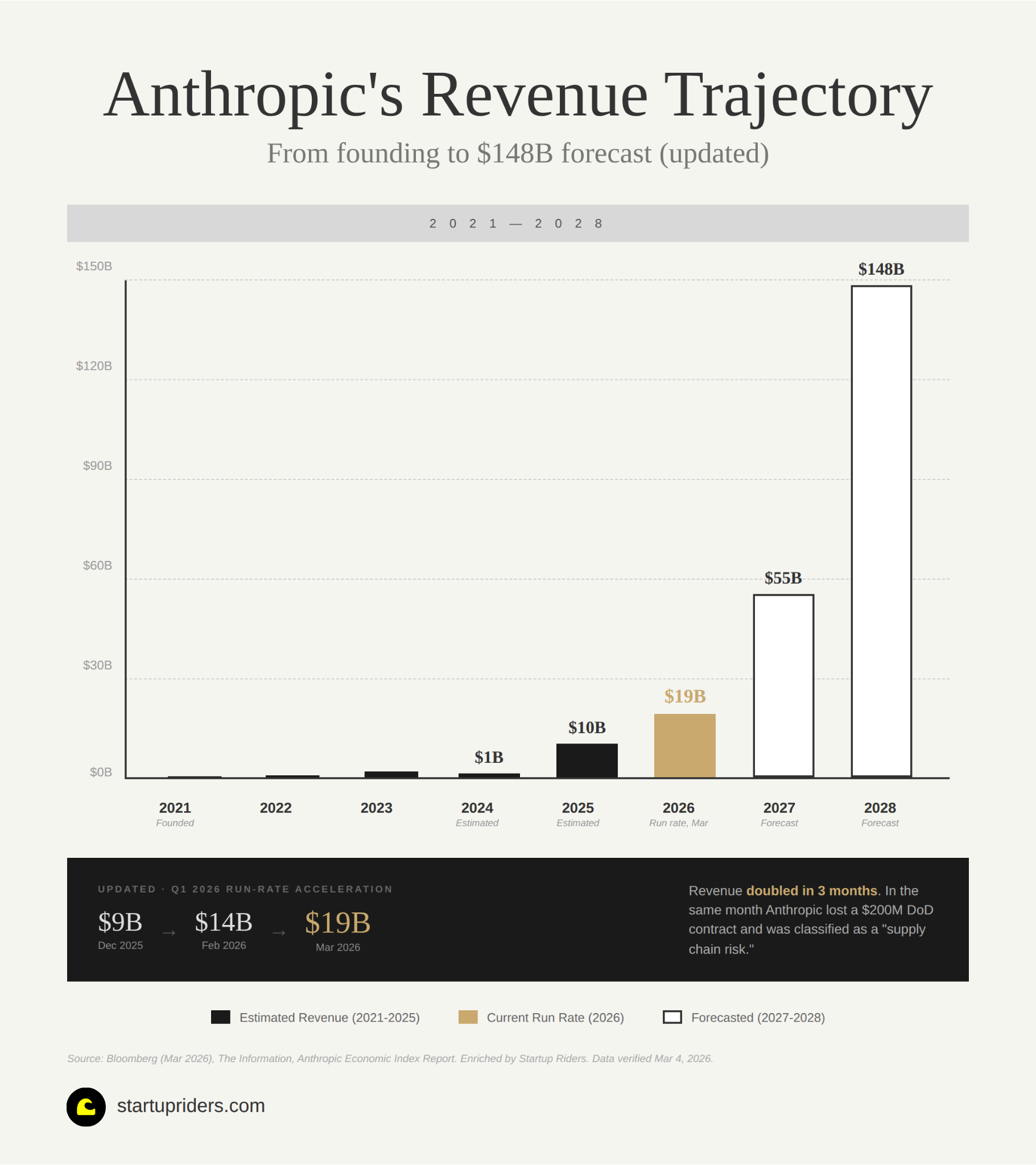

3. Anthropic's run rate: $9B (Dec) → $14B (Feb) → $19B (Mar).

The revenue growth story is unprecedented.

The details

Bloomberg reported this week that Anthropic’s annualised revenue run rate just hit $19 billion:

$9B at end of 2025

$14B in February 2026

$19B in early March 2026

So what

This rate of adoption is driven mostly by Claude Code and enterprise API adoption. There’s also a good question (for another time) to dig on here which is the speed at which people switch models (for the same use-case) and how enterprise sales cycles will affect their stickiness (and vice-versa).

4. 295% spike in ChatGPT uninstalls. Claude #1 on App Store for the first time.

In a multi-model world, trust becomes a product feature.